Benoit Mandelbrot's Fractal Insights on Navigating Financial Market Turbulence

23 June, 2024

Benoit Mandelbrot, a Polish-born, French, and American mathematician, profoundly impacted our understanding of markets and investing. Known for his broad interests in practical sciences, Mandelbrot's work, alongside Richard Hudson, in "The Misbehavior of Markets: A Fractal View of Financial Turbulence," provides a revolutionary perspective on financial systems. This article aims to distill Mandelbrot’s ideas into accessible insights for non-experts, highlighting the practical implications of his theories on modern investing and financial policy. Mandelbrot's ideas, while complex, offer a valuable lens through which we can better understand the inherent turbulence in financial markets.

The Nature of Market Randomness

Wild vs. Mild Randomness

Mandelbrot categorizes market randomness into three distinct types: wild, mild, and slow. He uses analogies to describe these types:

- Wild randomness: Comparable to the gaseous phase of matter, it is characterized by high energy, lack of structure, and unpredictability. This is the state where market price fluctuations are extreme and often unexpected.

- Mild randomness: Analogous to the solid phase, it involves low energy, stability, and predictability. Here, price changes are minimal and expected.

- Slow randomness: Resembling the liquid phase, it is intermediate, with more fluid but still somewhat predictable changes.

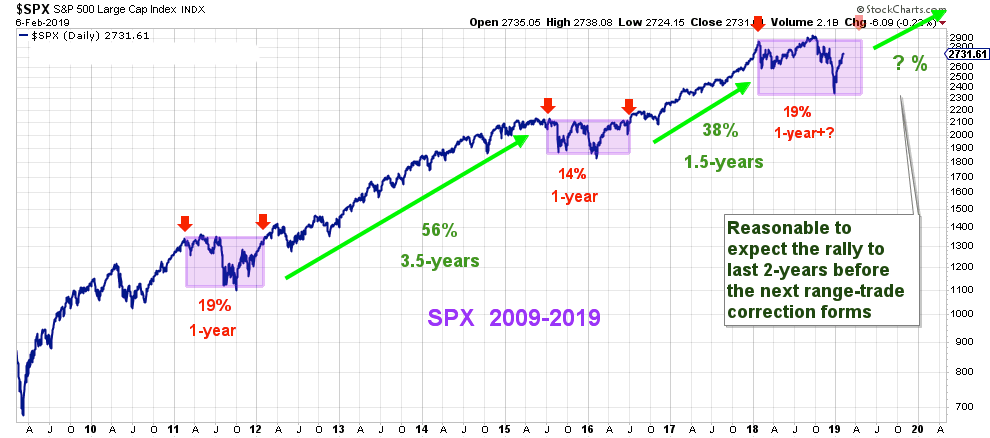

Mandelbrot asserts that real markets exhibit wild randomness. The fluctuations in prices can be substantial and damaging, contradicting the mild variations predicted by orthodox finance models. This has significant implications for portfolio construction and risk management. For example, during the financial crisis of 2008, the extreme price swings highlighted the inadequacies of conventional risk models.

Fractals and Market Patterns

Understanding Fractals

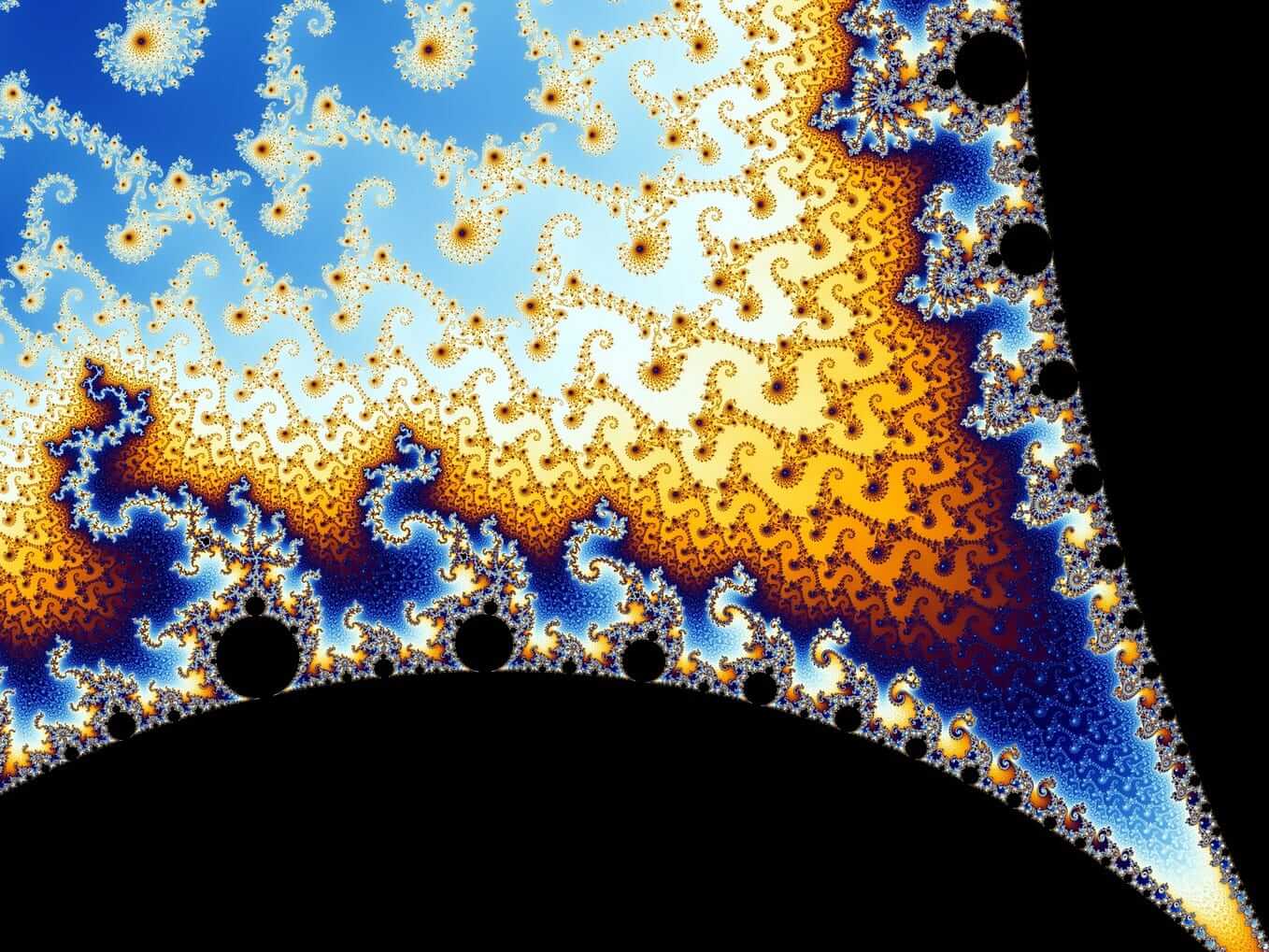

Fractals, a term coined by Mandelbrot, describe geometric shapes that can be subdivided into parts, each of which is a reduced-scale version of the whole. In finance, this concept translates to the observation that market movements at different timescales look similar when adjusted for scale. This self-similarity is a cornerstone of fractal theory.

Fractals demonstrate that market behavior at a daily level mirrors the patterns observed over longer periods, such as weeks or months. This insight helps investors understand that short-term and long-term market behaviors are not fundamentally different but rather scaled versions of each other.

Practical Implications

Fractal mathematics does not predict specific outcomes but indicates that extreme events are inevitable. Investors should prepare for these occurrences rather than rely on models that assume a normal distribution of returns. Robert Hagstrom, in "Investing: The Last Liberal Art," emphasizes that one must be ready for these outcomes, reinforcing the notion that wisdom in investing often means acknowledging what cannot be predicted. For instance, during the dot-com bubble burst, the fractal nature of market declines became evident as short-term crashes mirrored longer-term market downturns.

Critique of Conventional Financial Models

The Danger of Ignoring Large Price Changes

Mandelbrot was critical of traditional financial models that rely on Gaussian distributions and other simplifying assumptions. These models often ignore the possibility of large, sudden price changes, leading to underestimation of risk. For instance, the failure of Long-Term Capital Management in 1998 and the collapse of Enron in 2001 are stark reminders of the dangers of such oversights. These events highlighted the inadequacy of models that did not account for extreme, unpredictable events.

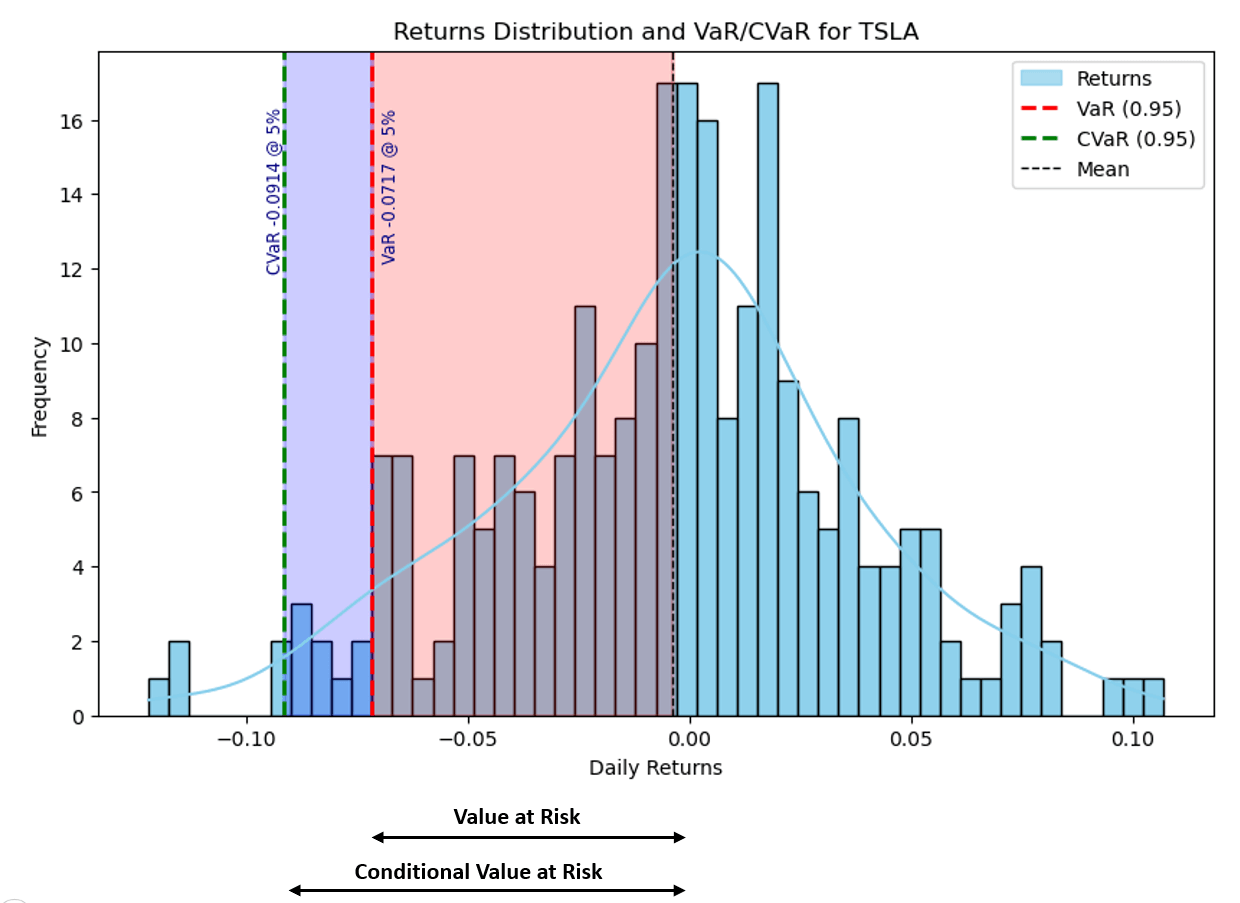

The Flaws in Risk Metrics

Standard risk metrics like beta, standard deviation, and the Sharpe ratio fail to capture the true risk of large deviations. Mandelbrot, along with Nassim Taleb, argued that these measures disregard the significant impact of rare, extreme events on long-term returns.

Table 1: Comparison of Risk Metrics

| Metric | Description | Limitation |

|---|---|---|

| Beta | Measures volatility relative to the market | Ignores large, unexpected deviations |

| Standard Deviation | Measures average deviation from the mean | Assumes normal distribution of returns |

| Sharpe Ratio | Risk-adjusted return measure | Fails to account for non-normal distribution |

| Value at Risk (VaR) | Estimates potential loss over a period | Underestimates risk of extreme events |

These metrics, while widely used, often provide a false sense of security by smoothing over the volatility that can devastate portfolios during financial crises.

The Impact of Extreme Events

Joseph vs. Noah Effects

Mandelbrot distinguished between "Joseph" effects (gradual, continuous market changes) and "Noah" effects (sudden, catastrophic changes). Most financial models focus on Joseph effects, overlooking the profound impact of Noah effects. The financial turmoil following the 9/11 attacks exemplifies a Noah effect, where market closures and significant price drops had dramatic consequences. The sharp movements during such events underline the necessity of considering extreme risks in financial planning.

Concentration of Returns

A small number of outcomes drive the majority of financial returns. Professor Bessembinder's research shows that a tiny fraction of stocks is responsible for the net gain in the U.S. stock market since 1926. This positive skewness in returns means that most stocks underperform, highlighting the importance of diversification and recognizing the potential for extreme outcomes. Investors often fail to appreciate that their returns are driven by a handful of high-performing assets, emphasizing the need for a diversified approach.

The Networked World and Market Turbulence

Increased Interconnectedness

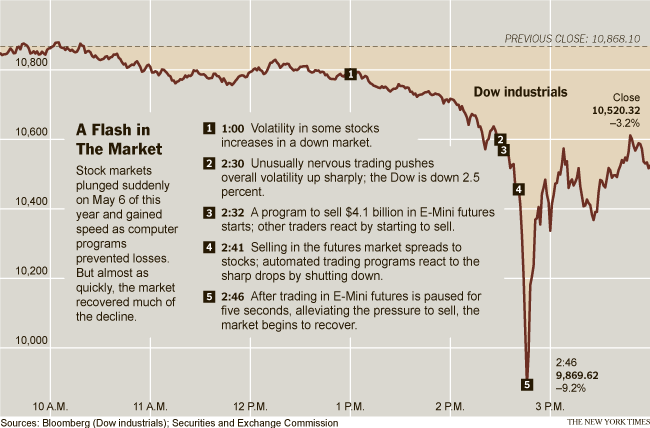

In today's interconnected world, market disturbances can propagate rapidly across global markets. The proliferation of technology and the digital economy has accelerated this phenomenon. The 2010 Flash Crash, where the Dow Jones Industrial Average plummeted and rebounded within minutes, illustrates the potential for instantaneous, widespread market chaos. This interconnectedness increases the complexity and unpredictability of market behavior, challenging traditional risk management practices.

The Role of Digital Assets

Digital assets like Bitcoin amplify these effects due to their inherent volatility and the speed at which information spreads in the digital age. The dramatic price swings of Bitcoin, often driven by speculative trading and market sentiment, underscore Mandelbrot's point about wild randomness and the limitations of conventional financial models. Bitcoin's fluctuations serve as a modern example of how traditional financial theories struggle to account for the behavior of emerging, highly volatile markets.

Human Nature and Pattern Recognition

The Desire for Order

Humans have an innate desire to find patterns and impose order on chaotic systems. This tendency can lead to the overinterpretation of random data, resulting in misguided investment decisions. Promoters of certain trading strategies exploit this cognitive bias to their advantage, selling the illusion of predictability. This desire for order often results in investors clinging to simplistic models that fail to capture the true complexity of financial markets.

The Illusion of Predictability

The brain’s tendency to highlight perceived patterns and disregard contradictory information can lead to erroneous conclusions. For instance, the Elliot Wave Theory claims to predict market movements based on observed patterns. However, Mandelbrot emphasized that market behavior is more accurately described by complex adaptive systems, which are inherently unpredictable. This distinction is crucial for investors to understand, as it underscores the futility of attempting to predict market movements with absolute certainty.

Practical Takeaways for Investors

Accepting the Uncertainty

Investors must accept that markets are unpredictable and that extreme events will occur. This means adopting strategies that are robust to uncertainty, such as diversification and maintaining a margin of safety. Recognizing the limitations of traditional financial models is crucial for effective risk management. Strategies that are resilient to market shocks, like holding a mix of asset classes, can help mitigate the impact of unpredictable events.

Preparing for Extremes

Given the inevitability of extreme events, investors should focus on preparation rather than prediction. This involves stress-testing portfolios against various scenarios and avoiding over-reliance on historical data that may not capture future risks. Taleb’s concept of "antifragility" – systems that thrive under volatility – is a valuable framework in this regard. Implementing antifragile strategies can help investors benefit from market volatility instead of being harmed by it.

Conclusion

Benoit Mandelbrot's ideas challenge conventional wisdom in finance, emphasizing the importance of recognizing wild randomness and the limitations of traditional models. His work underscores the need for a paradigm shift in how we understand and manage financial risk. By embracing the fractal nature of markets and preparing for extreme events, investors can navigate the turbulent financial landscape more effectively. Mandelbrot's insights encourage a deeper appreciation of market complexity and the necessity of robust, adaptable investment strategies.

Incorporating Mandelbrot’s insights into investment strategies requires a fundamental shift in thinking, moving away from the false security of traditional models and towards a more nuanced understanding of market behavior.