ETF Arbitrage Trading Strategy with Python

1 May, 2024

Exchange-Traded Funds (ETFs) offer a unique opportunity for arbitrage due to the nature of their design and trading mechanisms. ETF arbitrage involves capitalizing on price discrepancies between an ETF and its underlying assets. This article will explore the theory behind ETF arbitrage and demonstrate how to implement a basic arbitrage strategy using Python.

The Theory Behind ETF Arbitrage

ETFs are designed to track the performance of an index, commodity, or a basket of assets. They trade on exchanges similar to stocks, allowing their prices to fluctuate throughout the trading day. However, the price of an ETF should, in theory, be closely aligned with the Net Asset Value (NAV) of its underlying assets. This is because the ETF structure allows for the continuous creation and redemption of shares, which helps maintain the market price near the ETF's NAV.

When the market price of an ETF deviates from its NAV, an arbitrage opportunity arises. This discrepancy is known as the "premium" or "discount" of the ETF. If the ETF trades at a discount to its NAV, arbitrageurs can profit by buying the ETF shares and redeeming them for the underlying assets at a higher value. Conversely, if the ETF trades at a premium, arbitrageurs can create new ETF shares by delivering the underlying assets to the ETF issuer and sell the ETF shares in the market at a higher price.

The Role of Authorized Participants (APs)

Authorized Participants (APs) play a crucial role in the ETF ecosystem. APs are financial institutions, typically large broker-dealers or market makers, that have the ability to create and redeem ETF shares. This process helps to keep the ETF's market price in line with its NAV.

When an ETF trades at a discount to its NAV, APs can buy the ETF shares and redeem them for the underlying assets at a profit. This process reduces the supply of ETF shares, which in turn, increases the ETF's market price until it aligns with the NAV. Conversely, if the ETF trades at a premium, APs can create new ETF shares by delivering the underlying assets to the ETF issuer and sell the ETF shares in the market at a higher price. This process increases the supply of ETF shares, which reduces the ETF's market price until it aligns with the NAV.

The ability of APs to create and redeem ETF shares is a key factor that helps maintain the efficient pricing of ETFs. This arbitrage mechanism ensures that the ETF's market price remains close to its NAV, allowing investors to benefit from the ETF's diversification and liquidity1.

Implementing the Strategy in Python

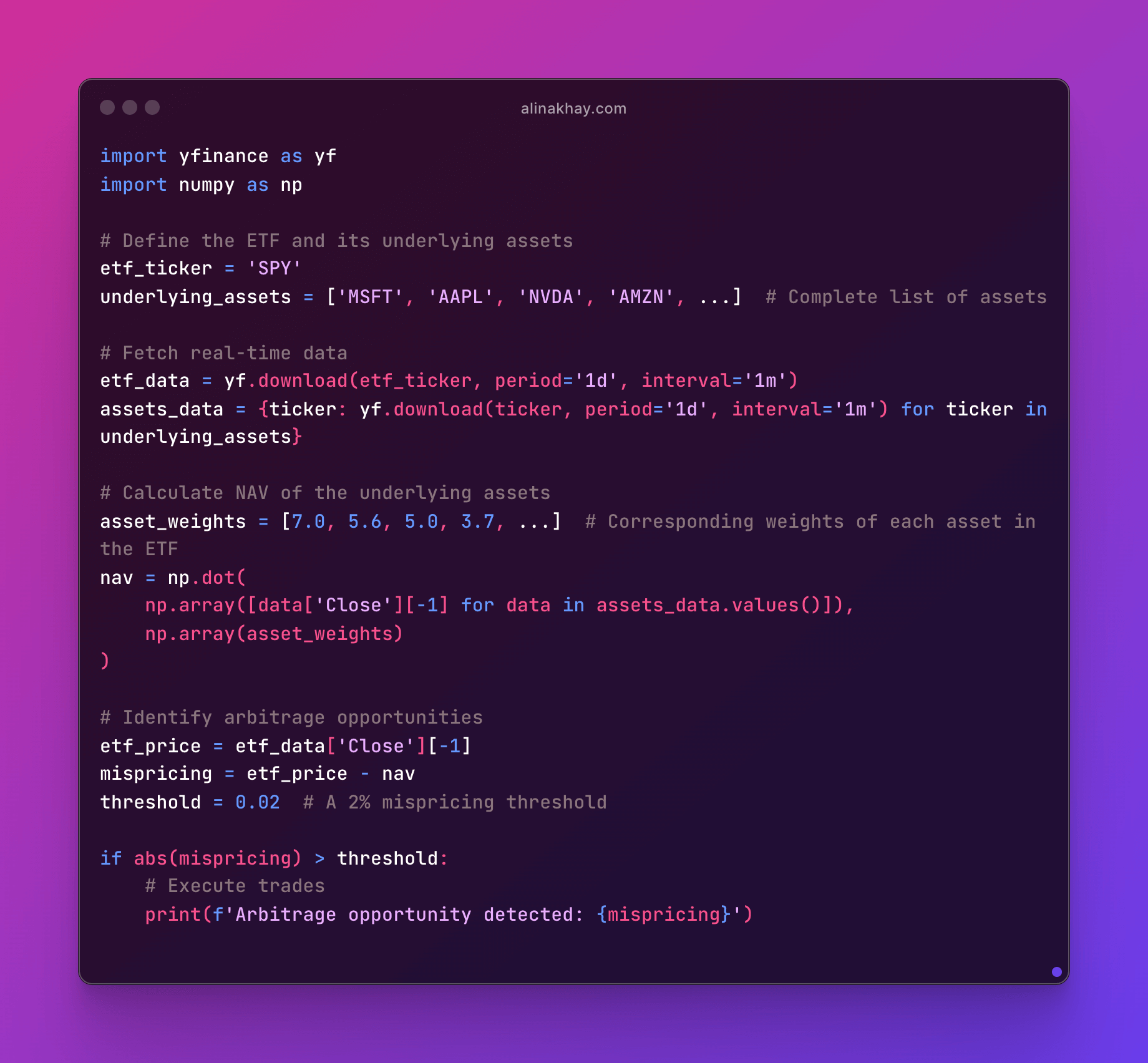

To implement an ETF arbitrage strategy, we need to:

- Monitor the ETF and its underlying assets: We need real-time data to identify when the ETF's market price diverges significantly from its NAV.

- Calculate the arbitrage opportunity: Determine the size of the discrepancy and whether it's large enough to cover transaction costs and potential risks.

- Execute trades swiftly: If an opportunity is identified, execute the trades quickly before the market corrects the mispricing.

Here's a simplified Python code snippet that demonstrates these steps:

ETF arbitrage is a sophisticated strategy that requires access to real-time market data and the ability to execute trades rapidly. While the above Python code is a basic representation, a practical implementation would involve more complex considerations such as transaction costs, market impact, and risk management.

Selling SPY Options

In addition to ETF arbitrage, selling options on ETFs like SPY can be part of a systematic trading strategy. Options selling strategies, like writing covered calls or selling cash-secured puts on the ETF can generate additional income and potentially enhance the overall returns of the ETF arbitrage portfolio.

Writing covered calls involves selling call options on the ETF shares that the trader already owns as part of the arbitrage positions. By selling the call options, the trader collects the option premium, which can provide a consistent source of income. If the ETF's price remains below the strike price of the call option, the option will expire worthless, and the trader gets to keep the premium. However, if the ETF's price rises above the strike price, the option may be exercised, and the trader would have to sell the ETF shares at the strike price, potentially limiting the upside of the arbitrage positions.

Selling cash-secured puts on the ETF can also be integrated into the ETF arbitrage strategy. In this case, the trader collects the option premium and agrees to buy the ETF at the put option's strike price if it is exercised. If the ETF's price remains above the strike price, the put option will expire worthless, and the trader keeps the premium. However, if the ETF's price falls below the strike price, the trader may be obligated to purchase the ETF shares at the strike price, potentially exposing them to downside risk in the arbitrage positions.

By combining these options selling strategies with the core ETF arbitrage approach, traders can potentially generate additional income and enhance the overall profitability of their trading activities. The options selling strategies can provide a steady stream of cash flows, which can be used to offset any potential losses or costs associated with the arbitrage positions.

Conclusion

Combining ETF arbitrage with systematic options selling strategies can create a diversified approach to trading. Both strategies require discipline, a solid understanding of market mechanics, and the ability to respond quickly to market opportunities. By leveraging Python for automation and real-time data analysis, traders can enhance their ability to identify and capitalize on these opportunities.

The key benefits of this combined approach include.

- Diversification. Combining ETF arbitrage and options selling strategies can provide diversification, reducing the overall risk of the trading portfolio.

- Income Generation. The options selling strategies can generate consistent income, which can complement the opportunistic nature of ETF arbitrage.

- Enhanced Returns. If executed properly, the combined strategies can potentially enhance the overall returns of the trading portfolio.

However, it's important to note that these strategies also have significant drawbacks:

- Complexity. Both ETF arbitrage and options trading require a deep understanding of market dynamics and sophisticated risk management techniques.

- Execution Risk. Timely execution of trades is crucial, as any delays can lead to missed opportunities or increased losses.

- Exposure to Market Risks. While diversification can mitigate some risks, the trading portfolio remains exposed to overall market movements and volatility.

Implementing these strategies successfully requires extensive research, robust backtesting, and a well-designed risk management framework. Traders should carefully evaluate their risk tolerance, financial resources, and trading experience before deploying these strategies.