Exposing Market Anomalies: The Role of Retail Trading in Momentum Profits

30 May, 2024

Retail trading, driven by individual investors buying and selling stocks, has a significant impact on market dynamics. Despite their smaller trading volumes, retail traders can influence stock prices and hence contibute to market anomalies. This article delves into the relationship between retail trading and momentum profitability, investigating whether stocks with higher levels of retail trading exhibit stronger momentum effects, offering valuable insights for both academics and practitioners.

Retail Trading and Market Anomalies

Retail investors, often less sophisticated than institutional investors, exhibit behavioral biases that can lead to market anomalies—situations where stock prices deviate from their fundamental values. One such anomaly is momentum trading, a strategy that buys past winners and sells past losers. Historically, momentum strategies have generated significant excess returns, challenging the notion of market efficiency. Recent studies have shown that retail investors' contrarian behavior around news events contributes to these momentum profits.

Hypotheses

We can come up with three three hypotheses regarding the relationship between retail trading and momentum profitability. These hypotheses are designed to uncover the underlying mechanisms through which retail investor behavior influences momentum trading outcomes:

- Hypothesis 1: There is a positive relationship between the current level of retail trading and future momentum profits.

This hypothesis posits that increased retail trading activity in the present can predict higher momentum profits in the future. The rationale is that retail investors, often driven by trends and market sentiment rather than fundamental analysis, can create price momentum by collectively buying or selling certain stocks, thereby pushing their prices further in the same direction. - Hypothesis 2: Retail investors prefer stocks with lottery-like characteristics, which amplifies momentum profits.

Lottery-like stocks are typically characterized by low prices, high volatility, and the potential for large payoffs. Retail investors, attracted by the possibility of substantial returns, tend to disproportionately invest in these stocks. This behavior can lead to significant price movements, enhancing the profitability of momentum strategies that capitalize on these trends. - Hypothesis 3: Stronger comovements among lottery-like stocks enhance momentum profits.

This hypothesis suggests that when lottery-like stocks move in tandem, driven by collective retail investor behavior, the momentum effect is magnified. Comovements can occur due to shared characteristics or simultaneous reactions to market news and sentiment. When these stocks exhibit correlated price movements, momentum traders can exploit the predictability of these trends to achieve higher returns.

Data and Methodology

The study utilizes data from the NYSE ReTrac database, covering retail trading from April 2005 to December 2015. Retail trading proportion (RTP) is calculated as the ratio of retail trading volume to total market trading volume. The formula for RTP is:

RTPi = Retail Trading Volumei / Total Market Trading VolumeiThe momentum strategy involves sorting stocks based on their past returns and retail trading levels.

Results and Analysis

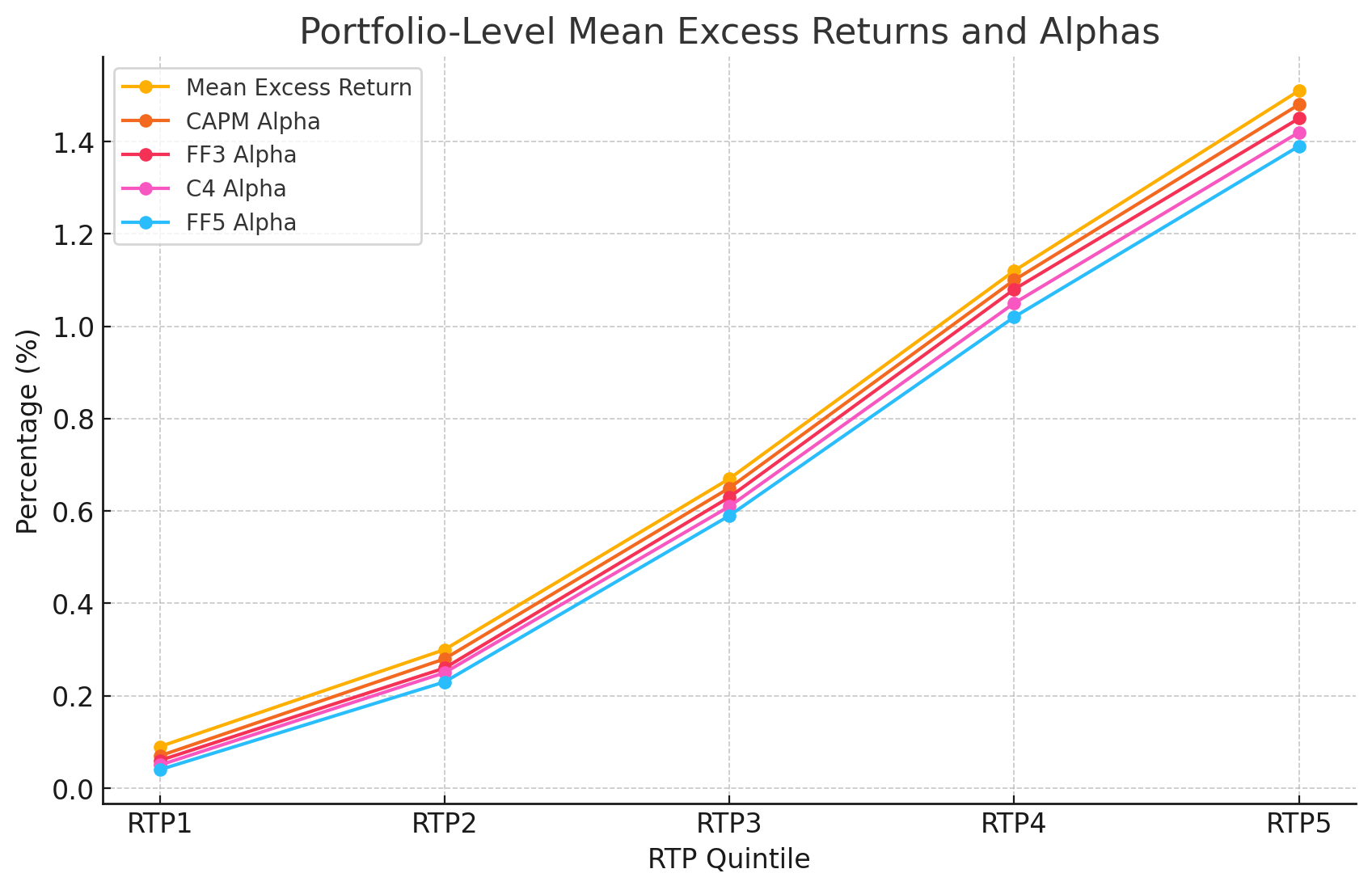

Stocks are sorted into quintiles based on RTP and past returns (Mom). Table 1 summarizes mean excess returns and alphas for the portfolios from April 2005 to December 2015. Results indicate a positive relationship between RTP and momentum profitability, with stocks in the highest RTP quintile exhibiting significantly higher momentum profits.

Table 1: Portfolio-Level Mean Excess Returns and Alphas

| RTP Quintile | Mean Excess Return | CAPM Alpha | FF3 Alpha | C4 Alpha | FF5 Alpha |

|---|---|---|---|---|---|

| RTP1 | 0.09% | 0.07% | 0.06% | 0.05% | 0.04% |

| RTP2 | 0.30% | 0.28% | 0.26% | 0.25% | 0.23% |

| RTP3 | 0.67% | 0.65% | 0.63% | 0.61% | 0.59% |

| RTP4 | 1.12% | 1.10% | 1.08% | 1.05% | 1.02% |

| RTP5 | 1.51% | 1.48% | 1.45% | 1.42% | 1.39% |

Figure 1: Portfolio-Level Mean Excess Returns and Alphas

Stock-Level Analysis

Using Fama and MacBeth (1973) regressions, the study examines the cross-sectional relationship between retail trading and future momentum profits. The results confirm that momentum effects are stronger among stocks with higher retail trading levels. A one standard deviation increase in a stock's past cumulative return leads to a 0.446 percentage points increase in the next month's return.

The Fama-MacBeth regression model is specified as:

Ri,t+1 = α + β1Momi + β2RTPi + β3(Momi × RTPi) + εi,t+1where Ri,t+1 is the return of stock i in month t+1, Momi is the past return, and RTPi is the retail trading proportion.

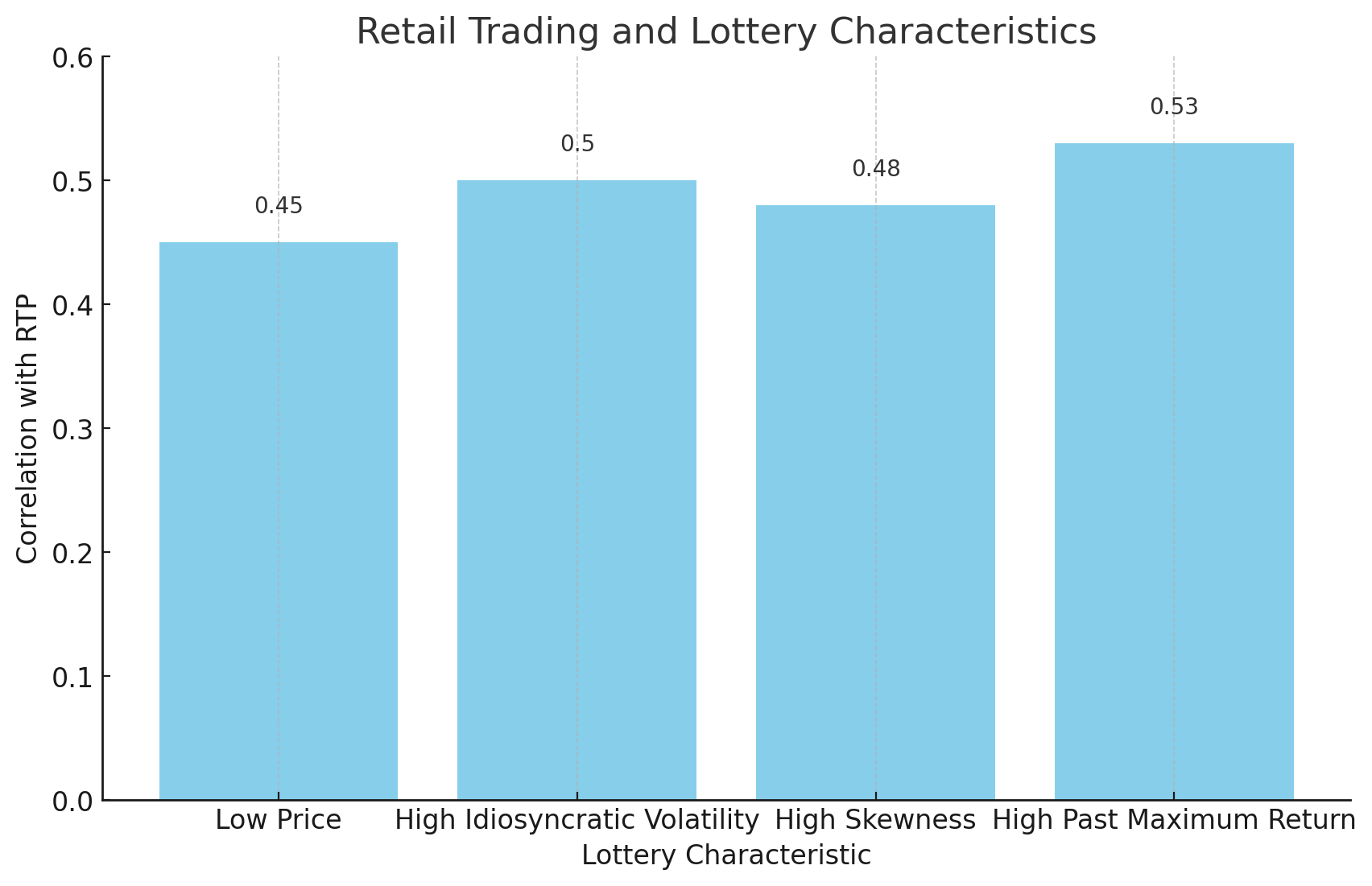

Retail Trading and Lottery Characteristics

Retail investors often favor stocks with lottery-like features such as low prices, high volatility, high skewness, and high past maximum returns. Table 2 shows the relationship between these characteristics and retail trading. Findings suggest a positive association, indicating that these lottery features amplify momentum profits.

Table 2: Retail Trading and Lottery Characteristics

| Lottery Characteristic | Correlation with RTP |

|---|---|

| Low Price | 0.45 |

| High Idiosyncratic Volatility | 0.50 |

| High Skewness | 0.48 |

| High Past Maximum Return | 0.53 |

Figure 2: Lottery Characteristics and Retail Trading

To ensure the robustness of the results, I replicate the analysis using data from the NYSE TAQ database for the same period. The findings are consistent, indicating a strong positive relationship between retail trading and momentum profits across different time periods and datasets.

Conclusion

In this study I study relationships between retail trader behaviour in trading momentum stocks and future returns profitability, providing evidence that retail trading amplifies momentum profitability. Stocks with higher levels of retail trading exhibit stronger momentum effects, driven by behavioral biases and a preference for lottery-like characteristics. These findings hold significant implications for understanding market anomalies and developing trading strategies.

For investors, particularly retail investors and fund managers, these insights can guide more effective portfolio construction. By recognizing the impact of retail trading on momentum, traders can better time their market entries and exits, potentially enhancing returns.

Future Directions

Given the rapidly evolving landscape of financial markets, further research could explore how technological advancements, such as algorithmic trading and AI-driven analytics, might influence the interaction between retail trading and momentum profitability. Additionally, understanding the regulatory impacts on retail trading behaviors could offer new strategies for both mitigating risks and exploiting market inefficiencies.

The relationship between retail trading and momentum profitability is intricate but vital for crafting winning investment strategies. Gaining a deep understanding of these market insights equips traders to deftly navigate the intricate landscape of modern financial markets.