Fintech Digital Solutions and Real World Applications of Finance Technology

12 June, 2024

In the ever-evolving world of finance, a disruptive force has emerged that is poised to reshape the industry as we know it – fintech. This captivating chapter will guide us through the labyrinth of fintech's influence, tracing its journey from digital innovation to regulatory integration.

At the very heart of this transformative phenomenon lies the synergistic marriage of finance and technology – a union that has captivated stakeholders from all corners of the financial ecosystem. From tech-savvy consumers craving unparalleled convenience to policymakers navigating the intricacies of regulatory integration, the allure of fintech is simply undeniable.

The numbers tell a remarkable story, painting a vivid portrait of fintech's meteoric rise. Since the tumultuous aftermath of the global financial crisis, fintech companies have soared to unprecedented heights, their market values quadrupling in the years that followed (He et al., 2017). Investment flows have surged, reaching a staggering $247.2 billion in 2021 alone – a testament to the sector's resilience and enduring appeal (KPMG, 2023).

But beneath the surface of these dazzling figures lies a deeper narrative, one of transformation and democratization. Fintech's arsenal of tools – from robo-advisors to chatbots – empowers financial institutions to streamline operations and elevate the customer experience. Bank of America's trailblazing chatbot, Erica, stands as a shining example of this revolution, ushering in a new era of personalized customer service.

Yet, perhaps fintech's most profound impact lies in its ability to level the financial playing field. By dismantling barriers based on economic status, fintech ensures that everyone has access to essential financial services. The result? A more inclusive financial landscape, characterized by seamless transactions, rapid data processing, and enhanced efficiency.

As we embark on this captivating exploration, we'll uncover a tapestry of innovation, from digital platforms to emerging technologies like blockchain and cryptocurrencies. Each use case sheds light on fintech's transformative potential, inviting researchers and practitioners alike to navigate the complexities of finance in the digital age.

| Fintech Innovations | Key Features | Examples |

|---|---|---|

| Risk Assessment and Management | - Real-time analysis of large datasets - Proactive identification of abnormal patterns - Enhanced security measures | - ML algorithms for fraud detection - Advanced encryption methods for data protection |

| Know Your Customer (KYC) | - Digital identity verification - Paperless authentication processes - Reduced verification costs and processing times | - India's Aadhaar system - Electronic KYC (e-KYC) solutions |

| Brand and Reputation Management | - Real-time transaction monitoring - Cybersecurity measures - Maintaining customer trust and loyalty | - Biometric authentication - NLP for fraud detection |

| RegTech Solutions | - Automation of compliance tasks - Data-driven reporting - Enhanced transparency and efficiency | - SEC's EDGAR database - Blockchain for regulatory reporting |

| Blockchain Technology | - Decentralization and transparency - Immutable ledger capabilities - Disruption across various industries | - Bitcoin and cryptocurrencies - Supply chain management applications |

Digital Payments and Transfers

Adoption and Growth

The adoption of digital payments has seen a remarkable increase globally, with 64.1% of adults now utilizing these services. In developing economies, usage has surged from 35% in 2014 to 57% in 2021. This growth spans various sectors, from small merchants to smallholder farmers, facilitated by widespread mobile phone and internet access.

| Year | Percentage of Adults Using Digital Payments | Global Average |

|---|---|---|

| 2014 | 35% | 42% |

| 2021 | 57% | 64.1% |

Sectoral Impact

Digital payments have revolutionized healthcare and retail sectors. For instance, remote healthcare facilities can now receive funds efficiently, reducing transaction costs and expanding service reach (World Health Organization, 2021). During the COVID-19 pandemic, U.S. online retail spending soared to $347 billion in the first half of 2020 (McKinsey & Company, 2020).

In China, the digital payment market is dominated by Alipay and WeChat Pay, controlling 92% of the market. This widespread adoption contrasts with Sweden, where cash transactions accounted for only 9% of total transactions by volume in 2020 (McKinsey & Company, 2020).

Financial Efficiency

Digital payments streamline transactions, significantly reducing costs associated with traditional payment mechanisms. According to Klein (2022), advanced payment infrastructures and data science algorithms have reduced transaction fees, allowing financial entities to reallocate resources more effectively.

International Remittances

Mobile money services like M-Pesa have revolutionized international remittances, with over $1 billion transacted monthly via mobile phones in Africa (GSMA, 2021). M-Pesa provides branchless banking services, including deposits, withdrawals, transfers, and access to credit (Ndung’u, 2018).

Digital Lending

Accessibility and Efficiency

Fintech has revolutionized lending by providing cost-effective alternatives to traditional financial institutions, which often exclude borrowers with limited credit history. Fintech lenders in the U.S. quadrupled their market share between 2010 and 2016 by processing mortgage applications faster (Fuster et al., 2019).

SME Lending

Small- and medium-sized enterprises (SMEs) have particularly benefited from fintech lending. In China, Ant Group's Alipay extends credit to rural areas underserved by traditional banks (Hau et al., 2019). Peer-to-peer (P2P) lending platforms also connect investors and borrowers directly, bypassing traditional banks (Lyons and Kass-Hanna, 2022).

Government Programs

During the COVID-19 pandemic, the U.S. Small Business Administration's Paycheck Protection Program (PPP) leveraged fintech to distribute funds, demonstrating the potential of digital lending in crisis management (Erel and Liebersohn, 2022).

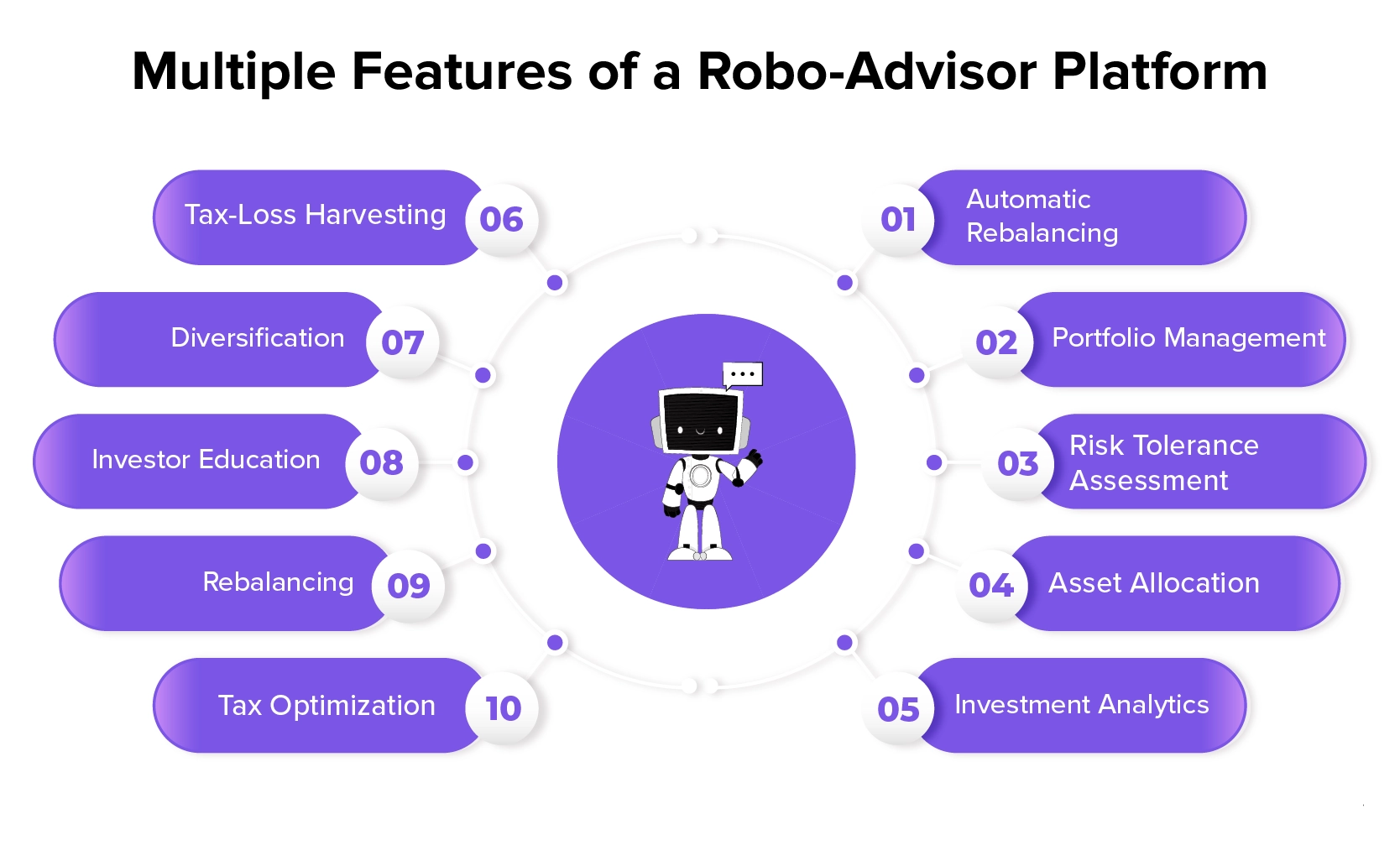

Digital Wealth Management

Robo-Advisors

Robo-advisors are transforming wealth management by offering automated, algorithm-driven investment services. These platforms provide cost-effective, transparent, and personalized financial advice, often at a fraction of the cost charged by human advisors.

| Service Type | Advisory Fee (% of AUM) |

|---|---|

| Human Advisors | 1-2% |

| Robo-Advisors | 0-0.5% |

Market Expansion

Robo-advisors cater to small investors who traditionally lacked access to wealth management services. Firms like Betterment and Wealthfront offer services with minimal investment requirements, democratizing access to financial markets (Bianchi et al., 2021).

Industry Adoption

The success of robo-advisors has attracted traditional financial institutions and high-tech companies, with global assets managed by robo-advisors projected to reach $2.76 trillion in 2023 (Statista, 2023). The shift towards digital wealth management is accelerating, driven by clients' preference for virtual advisory interactions (EY Global, 2023).

Digital Insurance/InsurTech

Innovations and Investments

The insurance industry has embraced fintech, with significant investments in insurtech companies like Lemonade and ZhongAn Insurance. These firms leverage big data, machine learning, and AI to enhance risk assessment and pricing models (Lin and Chen, 2020).

Data-Driven Risk Assessment

Insurtech firms utilize diverse data sources, including wearables, to gather biometric information for precise risk assessment. For instance, Lapetus Solutions uses video analysis to determine clients' health status and longevity (Lapetus Solutions, 2023).

Personalized Insurance Solutions

The integration of health data metrics with financial services enables insurers to offer personalized solutions, enhancing customer satisfaction and mitigating risks (Cortis et al., 2019).

The Impact of Fintech on Firm Management

Effective management lies at the heart of every successful financial institution. It dictates not only profitability and operational efficiency but also regulatory compliance and customer satisfaction. Poor management, conversely, can lead to substantial losses and systemic risks, as evidenced by historical events like the collapse of Lehman Brothers during the 2008 financial crisis. In response to these challenges, the integration of financial technology has emerged as a pivotal force in reshaping firm management practices, offering innovative solutions across various critical domains.

Enhancing Risk Assessment and Management

One of the foundational pillars where fintech has made significant strides is in risk assessment and management. Traditionally, financial institutions faced challenges in accurately assessing and mitigating risks, particularly operational risks stemming from fraud and market volatility. However, advancements in data analytics and machine learning have revolutionized this landscape. Fintech solutions now leverage sophisticated algorithms to analyze vast datasets in real-time, enabling proactive risk identification and management.

For instance, ML algorithms can detect abnormal transaction patterns indicative of fraudulent activities, thereby safeguarding institutions from potential financial losses. According to recent data, financial institutions have successfully reduced transaction data breach risks to as low as 2% through the adoption of advanced security measures. This not only bolsters financial security but also enhances operational efficiency by minimizing the time and resources spent on manual monitoring.

Revolutionizing Know Your Customer (KYC) Processes

Another critical area where fintech has made profound contributions is in Know Your Customer (KYC) processes. KYC requirements are vital for regulatory compliance and risk management, yet traditional methods often proved cumbersome and costly. The advent of digital identity verification and electronic KYC (e-KYC) solutions has streamlined this process dramatically.

Take, for example, India's Aadhaar system, which has revolutionized identity verification by allowing individuals to securely authenticate and share their electronic information without the need for physical documents. This innovation has not only reduced verification costs from $15.00 to $0.50 per customer but also slashed processing times from days to mere seconds (Allen et al., 2021). Such efficiencies are pivotal in promoting financial inclusion and facilitating seamless access to financial services for underserved populations.

Safeguarding Brand and Reputation Management

Maintaining a positive brand image and reputation is paramount for financial institutions, especially in today's digitally connected world where news travels fast. Fintech offers robust solutions for monitoring and managing brand integrity, including sophisticated cybersecurity measures and real-time transaction monitoring. These technologies not only detect and prevent fraudulent activities but also reassure customers of the institution's commitment to security and reliability.

Advancing Fraud Detection Capabilities

Fraud remains a persistent threat in the financial industry, ranging from unauthorized transactions to sophisticated phishing scams. Fintech innovations such as biometric authentication and natural language processing (NLP) have significantly bolstered fraud detection capabilities. Biometric authentication, for instance, enhances transaction security by verifying identities through unique biological traits, thereby mitigating the risks of identity theft and account takeovers (Hizam et al., 2021).

Moreover, NLP technologies analyze vast amounts of textual data to identify suspicious patterns indicative of fraudulent behavior, empowering institutions to preemptively combat financial crimes (Jain et al., 2023). These advancements underscore fintech's pivotal role in fortifying financial institutions' defenses against evolving threats while preserving customer trust and loyalty.

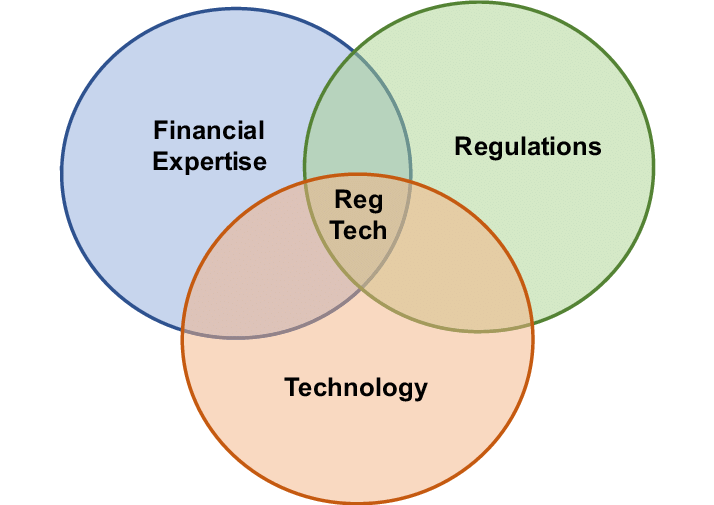

RegTech Innovating Regulatory Compliance

Regulatory compliance is a cornerstone of financial stability and consumer protection. However, navigating complex regulatory landscapes can be arduous and resource-intensive for financial institutions. Enter Regulatory Technology (RegTech), a burgeoning field that leverages technological solutions to streamline compliance processes and enhance regulatory outcomes.

Automating Compliance with RegTech

RegTech solutions automate regulatory compliance tasks, ranging from data management to reporting, thereby reducing human errors and operational costs associated with manual processes. Notably, systems like the U.S. Securities and Exchange Commission's EDGAR database have revolutionized regulatory filings by digitizing submission processes, enhancing transparency, and facilitating data-driven decision-making (U.S. Securities and Exchange Commission, 2023).

Conclusion

In conclusion, fintech represents a paradigm shift in firm management, empowering financial institutions with innovative tools to enhance operational efficiency, mitigate risks, and comply with stringent regulatory requirements. From revolutionizing KYC processes to fortifying cybersecurity measures and leveraging blockchain for transparent transactions, fintech continues to redefine the future of finance. As technology evolves and regulatory frameworks adapt, the integration of fintech solutions promises to usher in a new era of resilience, transparency, and customer-centricity in financial services.

In this article has explored how these technologies are not just reshaping operations but also ensuring financial institutions are well-equipped to navigate the complexities of a rapidly evolving global financial landscape.