How Stablecoins Are Fueling the Global Shift to Dollarization

17 February, 2025

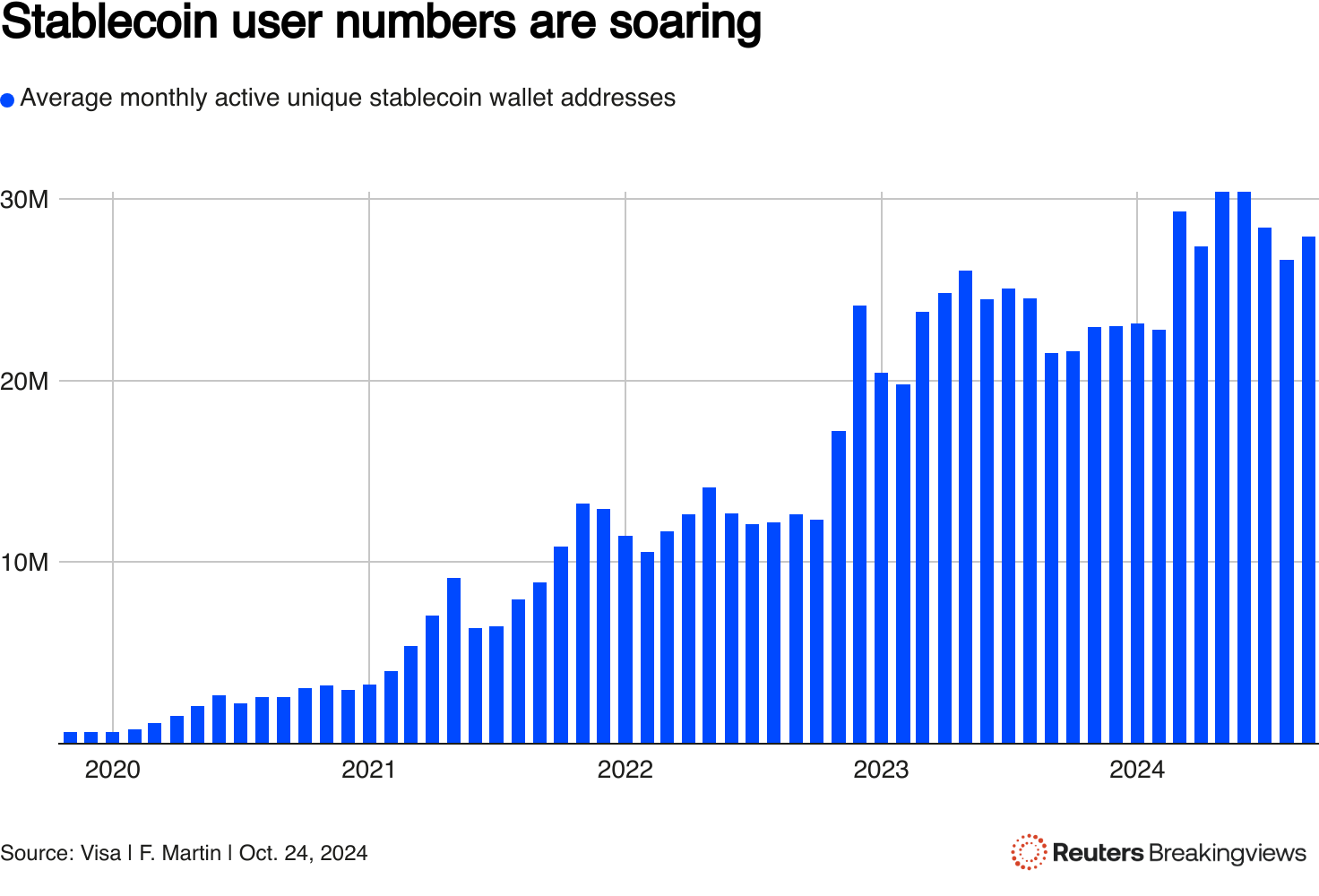

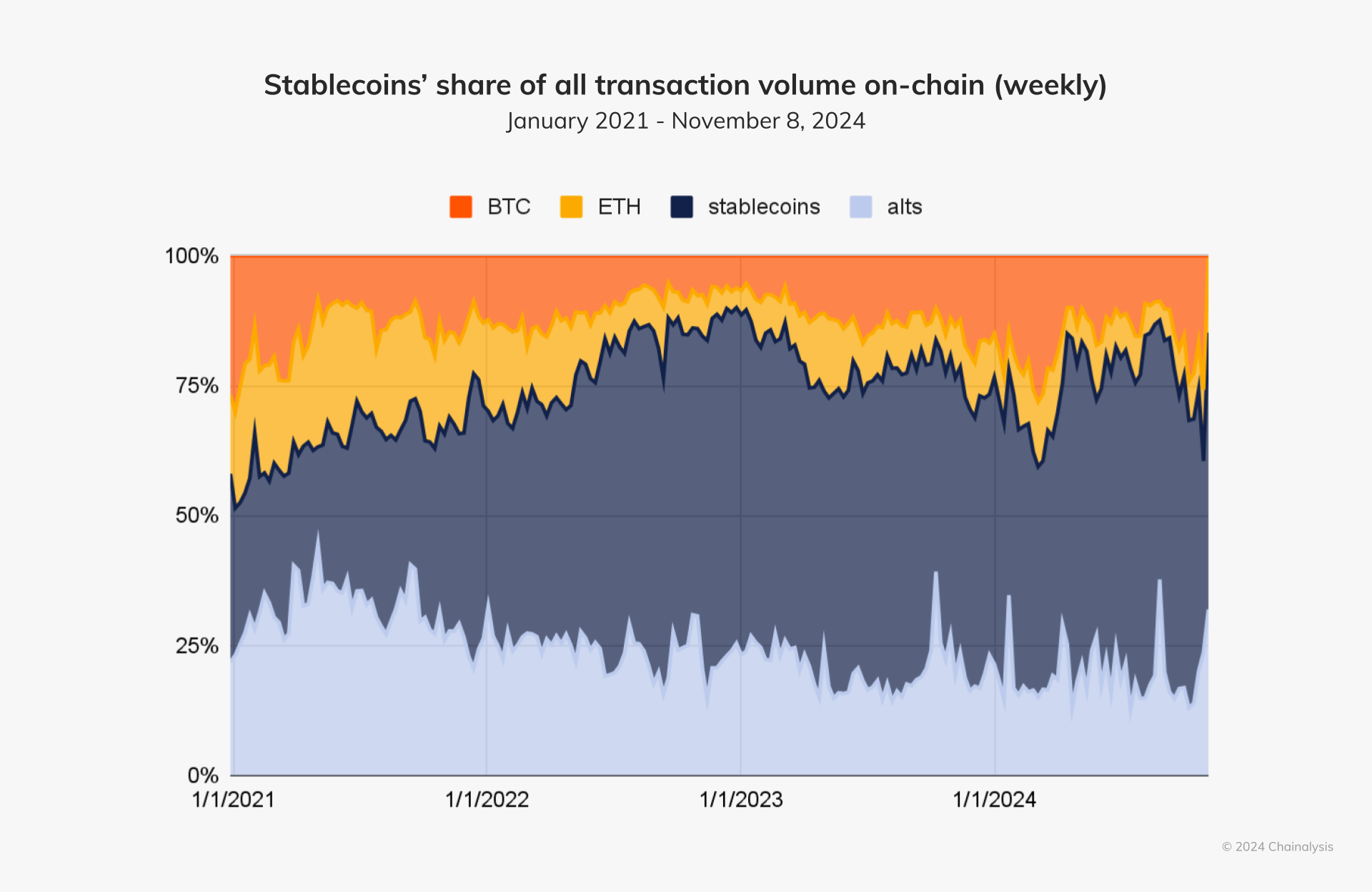

Stablecoins have quietly become a dominant force in the cryptocurrency market, blending the flexibility of digital assets with the stability of traditional fiat currencies. Unlike volatile cryptocurrencies, stablecoins maintain a predictable value, typically pegged 1:1 to fiat currencies such as the U.S. dollar. With adoption skyrocketing—usage is up 84% since August 2023, reaching a peak of $224 billion—stablecoins are reshaping global finance in ways that extend far beyond the crypto ecosystem. One of the most profound implications is their role in accelerating the dollarization of economies, especially in emerging markets. But why are stablecoins fueling this shift, and what are the broader economic consequences?

The Dollarization Effect

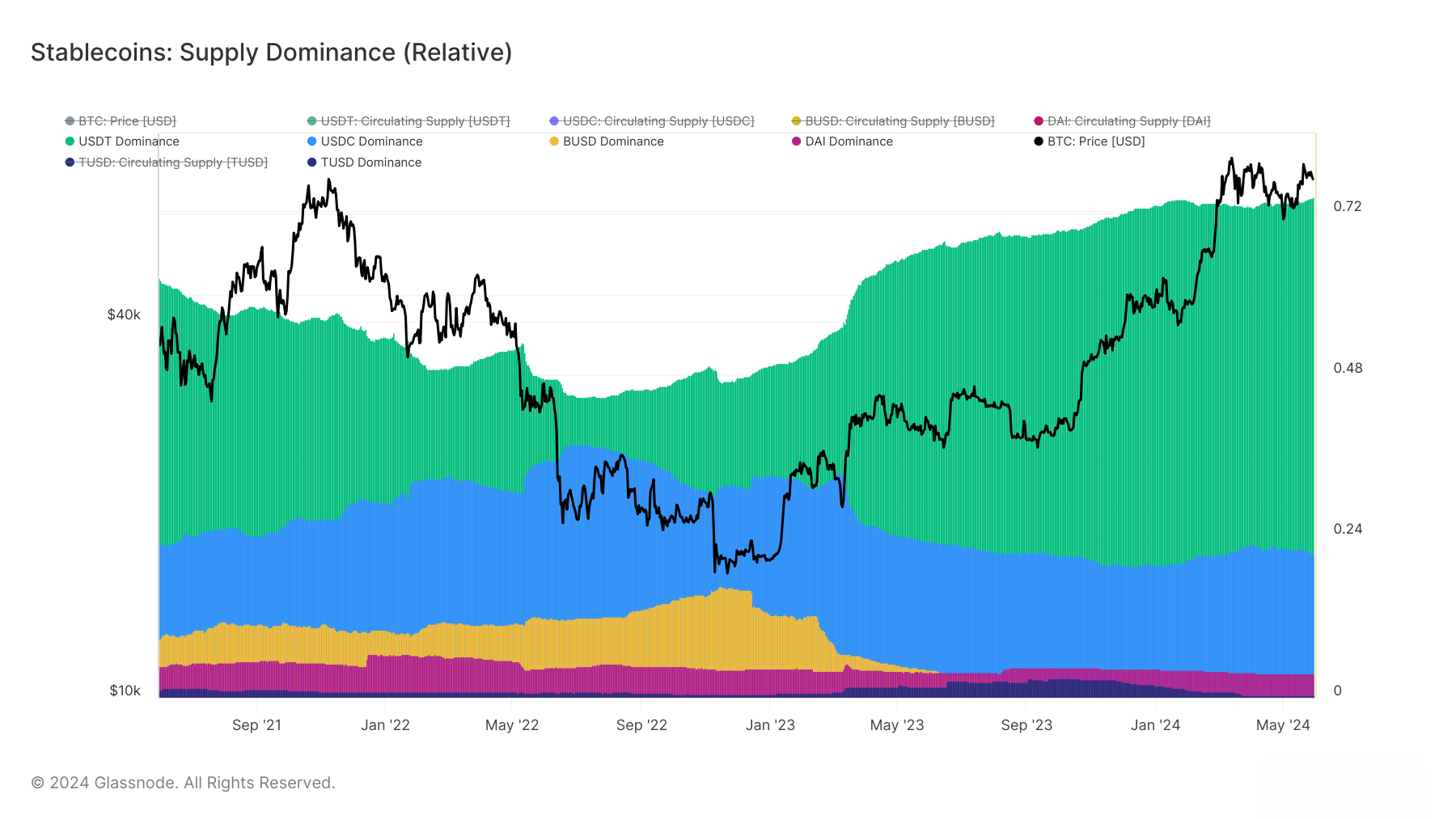

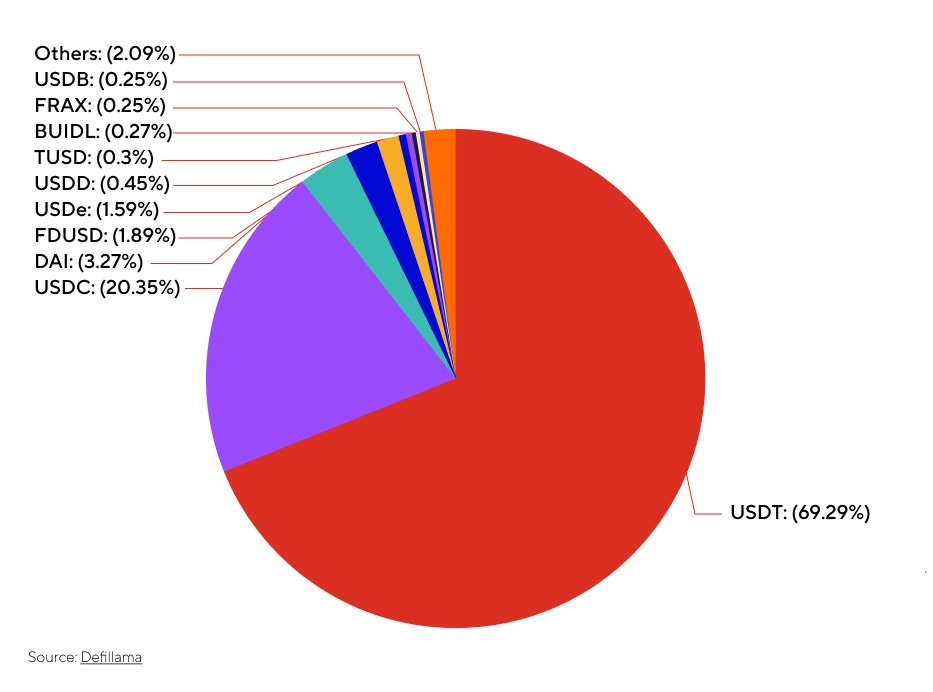

It is striking that nearly 99% of stablecoins, measured by market capitalization, are denominated in U.S. dollars—an astonishingly high share compared to traditional international trade and finance. This suggests that if monetary institutions were built from scratch today, the global market would overwhelmingly choose the dollar. In recent months, stablecoins have accounted for more than two-thirds (⅔) of the trillions of dollars worth of cryptocurrency transactions recorded worldwide. Their rise underscores the reality that global markets prioritize dollar stability when given a choice.

In countries with weak financial systems, unstable domestic currencies, or restrictive banking regulations, stablecoins offer an attractive alternative. They provide seamless, direct access to the global economy without relying on intermediaries, offering both individuals and businesses a more stable store of value and a more efficient means of transaction.

While this shift strengthens the dollar’s role in global finance, it does not necessarily benefit the institutions that uphold the current dollar system. By allowing individuals to access dollars and U.S. dollar-backed assets outside the traditional banking system, stablecoins bypass financial intermediaries that have historically controlled dollar distribution. This could accelerate episodes of crypto-dollarization, where weaker fiat currencies collapse as demand shifts overwhelmingly to stablecoins.

Why Emerging Markets are Embracing Stablecoins

Many traders and businesses in less well-governed economies want to conduct transactions in U.S. dollars, but limited access to dollar-based banking has traditionally posed a barrier. Some governments impose strict capital controls to discourage dollarization, while others face persistent inflation that erodes the value of their domestic currencies. Stablecoins provide an elegant workaround. By accessing stablecoins through decentralized apps, users can bypass traditional financial gatekeepers, avoiding excessive fees and slow processing times.

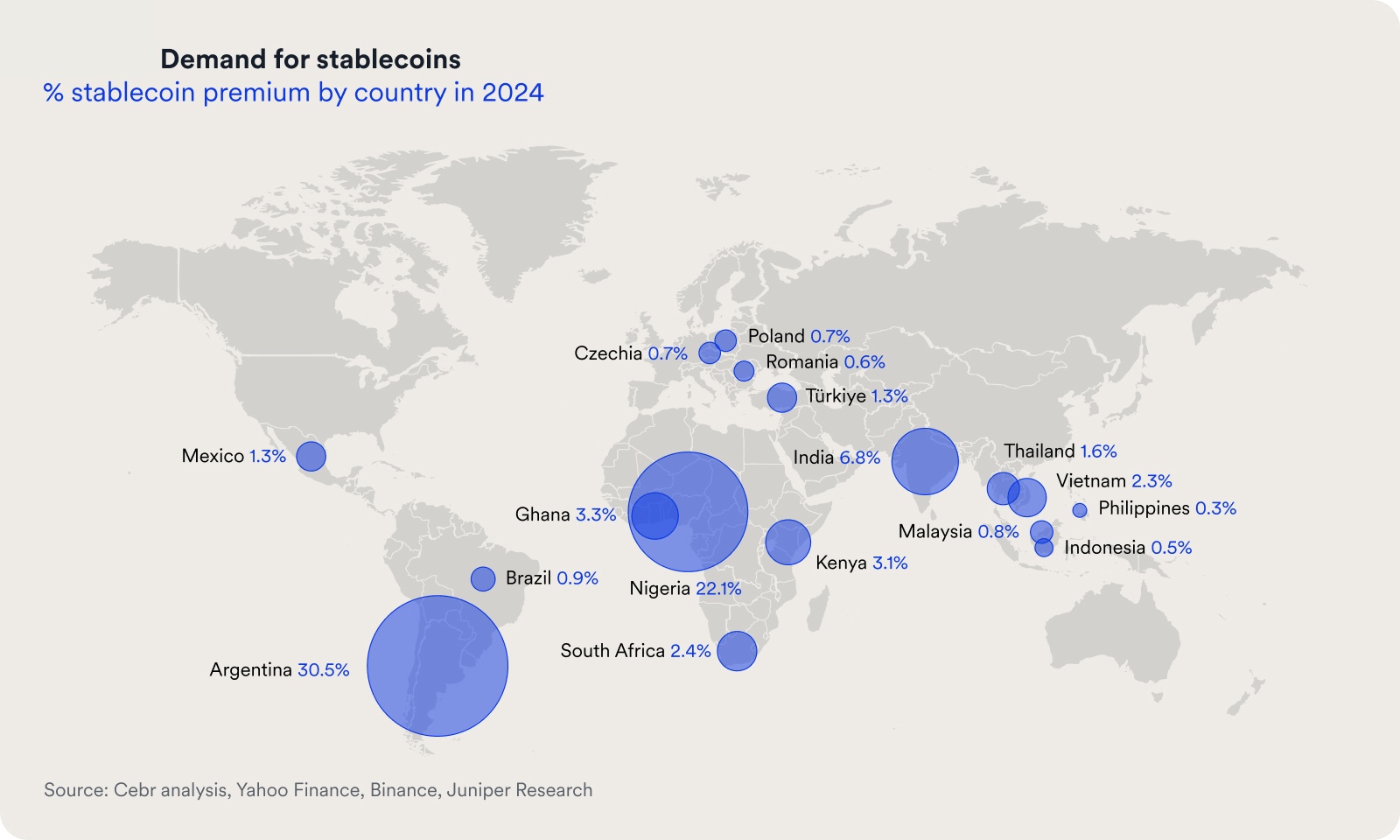

This trend is particularly pronounced in Latin America and Sub-Saharan Africa, where stablecoin usage for remittances, savings, and cross-border trade has surged by over 40% year-over-year. Eastern Asia and Eastern Europe are not far behind, seeing 32% and 29% growth in stablecoin transfers, respectively. Meanwhile, in Central & Southern Asia and Oceania, stablecoins play a crucial role in facilitating cross-border trade and bypassing traditional banking inefficiencies.

Almost 100 million addresses on-chain hold stablecoins today. They are increasingly being integrated into major payments networks, such as those run by Visa, Stripe, Checkout, PayPal, Worldpay, Nuvei, or MoneyGram, to name a few.

The Rise of Stablecoin-Powered Economies

As stablecoins become more embedded in everyday transactions, dual-currency economies are emerging. Individuals and businesses are increasingly thinking, pricing, and transacting in dollars via stablecoins, even when dealing domestically. Over time, the reliance on stablecoins can weaken the role of national currencies, leading to partial or full dollarization.

Countries like Panama, Ecuador, and El Salvador have already dollarized, and none seem to regret it. Argentina’s President Javier Milei has pledged to dollarize the country, a campaign promise that resonated deeply with citizens frustrated by decades of currency instability. In Nigeria and Turkey, retail adoption of stablecoins is soaring as users seek refuge from inflation and volatile exchange rates.

Beyond individual transactions, stablecoins are also driving new demand for the U.S. dollar itself. With an estimated $160 billion in net new dollar exposure, stablecoins function as a new liquidity channel that absorbs dollar assets, particularly short-term Treasuries and overnight repos, into the global crypto economy. If stablecoins continue their rise, they could become the dominant form of digital money worldwide—one that reinforces the dollar’s global standing while circumventing the financial institutions that have traditionally managed its reach.

Regulatory and Institutional Responses

Governments and financial regulators are taking notice. Some countries, like Singapore, are embracing stablecoins with regulatory frameworks to bolster confidence and transparency. The U.S. has intensified oversight of stablecoin issuers, with entities like Tether (USDT) and Circle (USDC) under increasing scrutiny. Tether, the largest stablecoin issuer, was fined $42 million in 2021 by the U.S. Commodity Futures Trading Commission for misrepresenting its reserves, but continues to dominate the market, holding nearly $100 billion in U.S. Treasury bills.

Meanwhile, stablecoin issuers have strengthened compliance efforts, working with regulators and leveraging blockchain analytics firms like Chainalysis to detect illicit activity. Most centralized stablecoin issuers now have the ability to freeze or burn tokens linked to criminal transactions, supporting global financial crime prevention.

The Future of Stablecoin-Driven Dollarization

The simplest scenario is that stablecoin adoption continues to expand, further entrenching the dollar as the dominant global currency. Retail adoption will likely persist in inflation-prone regions, while institutional players integrate stablecoins into liquidity management and international settlements.

However, regulatory uncertainty remains a challenge. Many governments fear losing control over monetary policy, and central banks are exploring Central Bank Digital Currencies (CBDCs) as a countermeasure. At the same time, stablecoins represent a fundamental shift in the way dollars circulate globally. Unlike the traditional dollar system, which is maintained by commercial banks and central bank reserves, stablecoins allow dollars to move seamlessly between individuals, businesses, and DeFi platforms—potentially diminishing the role of banks and central monetary authorities.

While concerns over regulation, redemption risks, and financial stability remain, the convenience and utility of stablecoins make them an increasingly indispensable part of the financial landscape. In the long run, stablecoins may pave the way for a world where economies voluntarily shift towards a digital-dollar standard, reshaping the global monetary order in ways yet to be fully understood.

Stablecoins are no longer just a niche financial tool—they are a powerful catalyst for global monetary evolution. Whether they ultimately strengthen or destabilize the global financial system remains to be seen, but one thing is clear: their impact is only just beginning.