Optimization in Algorithmic Trading

3 October, 2023

Optimization plays a crucial role in quantitative trading, where mathematical and computational techniques are used to make trading decisions. Quantitative trading, often referred to as algorithmic trading or quant trading, involves the use of quantitative models, statistical analysis, and historical data to identify profitable trading opportunities and manage risk.

Optimization algorithms start with an objective function that quantifies the trader's goals. In trading, this function typically involves maximizing returns and minimizing risk. The intuition here is to find a balance between making profits and avoiding losses.

Typical Scenarios for Optimization in Quantitative Trading

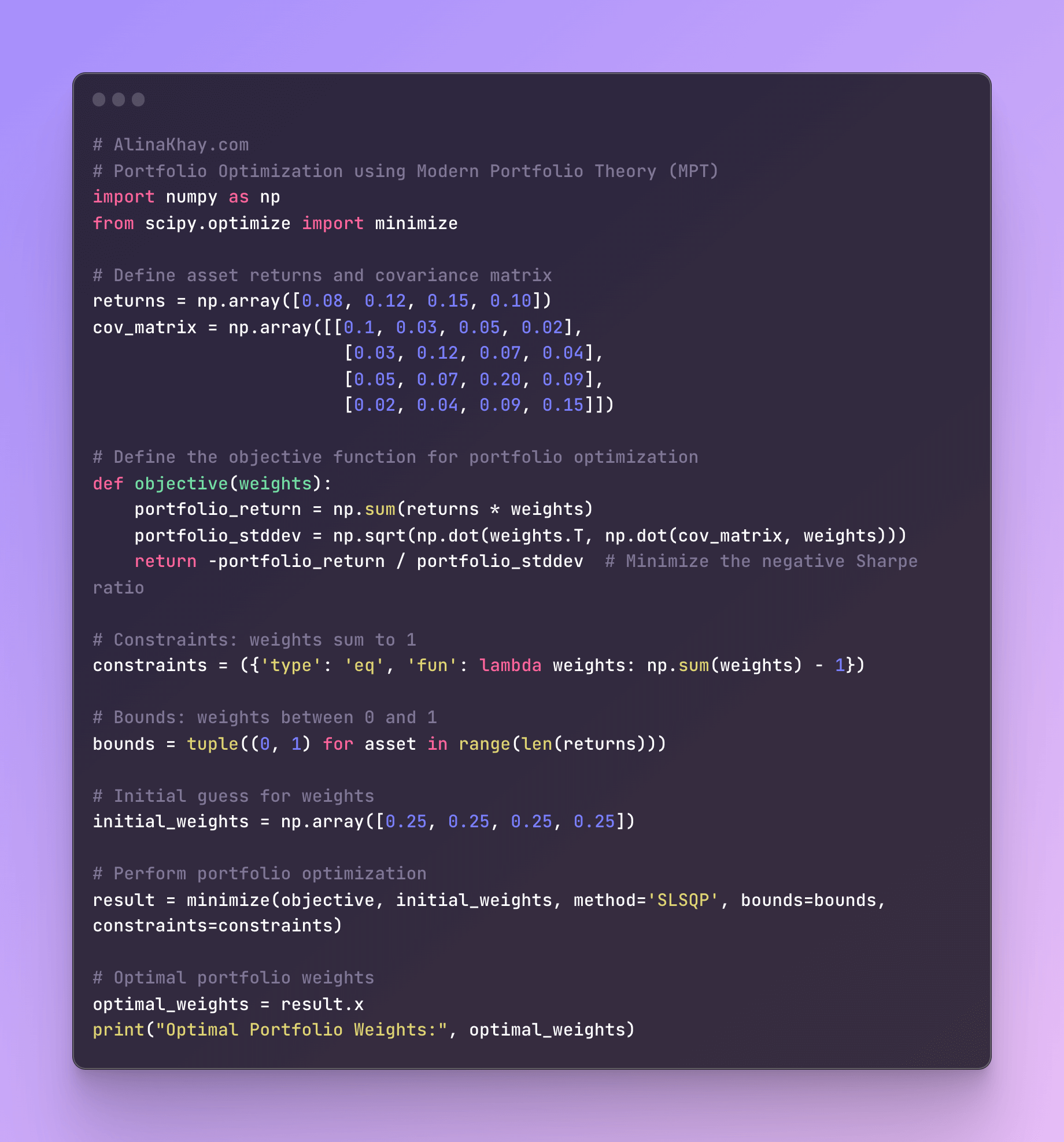

Portfolio Optimization

Portfolio optimization is a fundamental aspect of quantitative trading. It involves selecting a combination of assets or securities that maximize expected returns while minimizing risk. Optimization techniques like Markowitz's Modern Portfolio Theory (MPT) are commonly used to find the optimal allocation of capital among various assets.

The intuition behind diversifying the trading portfolio is that by spreading investments across different assets or asset classes, the risk can be reduced while maintaining the potential for returns.

Risk Management

Optimization is used to determine how much capital to allocate to different trading strategies or positions to manage risk effectively. Techniques like the Kelly Criterion help traders find the optimal bet size to maximize long-term portfolio growth while minimizing the risk of significant losses.

Strategy Parameter Tuning

Quantitative trading strategies often involve multiple parameters that can be adjusted to optimize performance. Optimization algorithms, such as grid search, genetic algorithms, or simulated annealing, are used to find the best combination of parameters to maximize profitability based on historical data.

The intuition behind optimization in this scenario is to find the optimal set of parameter values that result in the best trading performance. This is often done using historical data to backtest different parameter combinations.

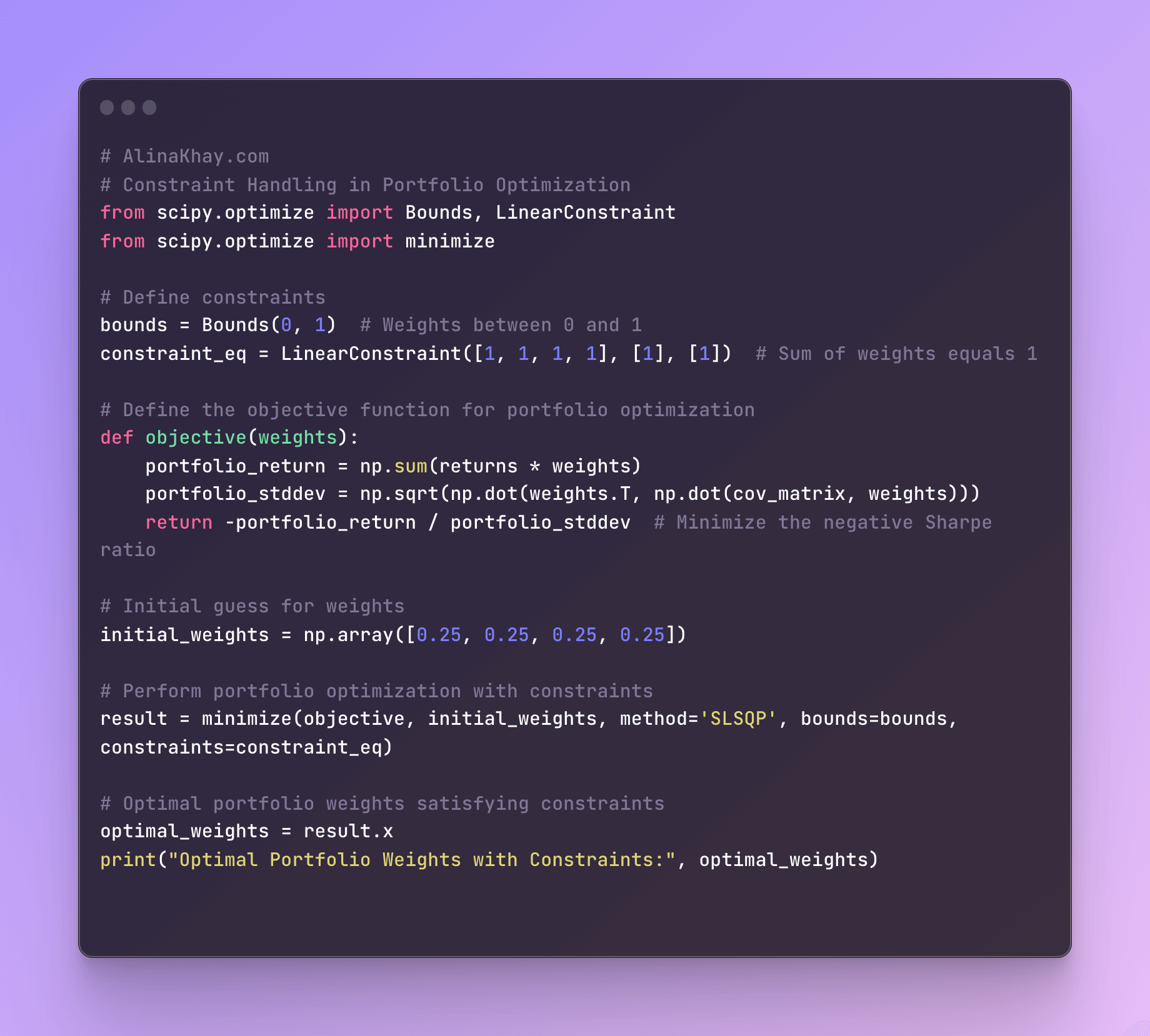

Constraint Handling

Optimization in quantitative trading often involves handling constraints such as regulatory limits, position size limits, and risk limits. Traders need to find solutions that meet these constraints while optimizing their objectives.

Order Execution

Optimizing order execution is crucial in minimizing trading costs, such as slippage and market impact. Algorithms are used to determine the best way to execute large orders without disrupting the market and to minimize trading costs.

Risk-Return Trade-offs

Quantitative traders use optimization to strike a balance between risk and return. They may optimize their strategies to achieve specific risk-return profiles, such as targeting a certain Sharpe ratio or maximum drawdown level.

Market Microstructure Optimization

Traders often optimize their strategies based on market microstructure factors, such as order book dynamics, liquidity, and trading volumes. These optimizations can help improve the timing and efficiency of trades.

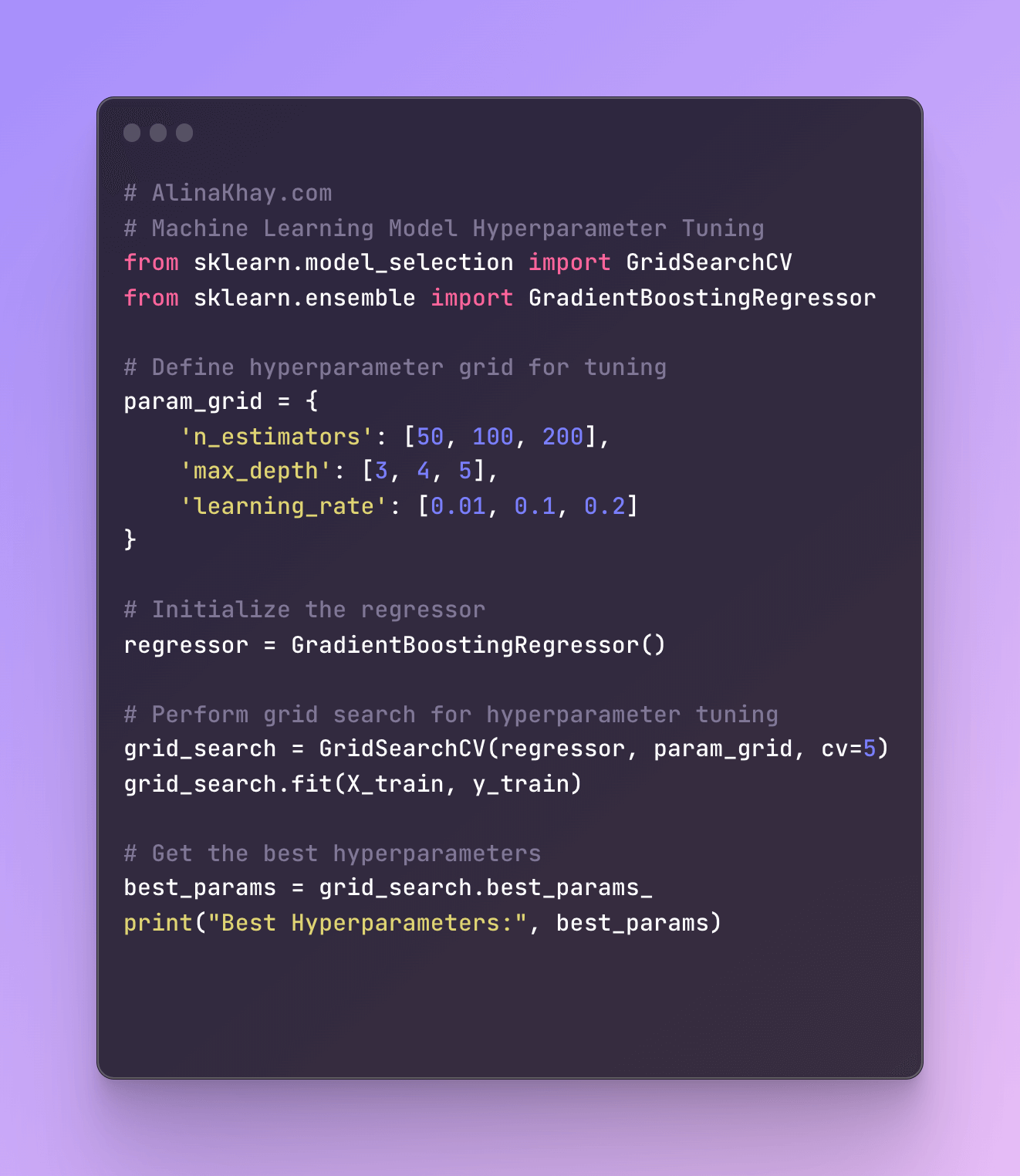

Machine Learning Model Optimization

In machine learning-based quantitative trading, optimization techniques are used to fine-tune model hyperparameters, select features, and optimize the overall model architecture to improve predictive accuracy and trading performance.

The intuition here is to leverage advanced computational methods to discover patterns and relationships in the data that human traders might miss.

Rebalancing

Portfolio rebalancing is a continuous process in quantitative trading, and optimization helps determine when and how to adjust portfolio allocations to maintain the desired risk-return profile.

High-Frequency Trading (HFT)

In high-frequency trading, optimization is used to optimize trading algorithms to execute orders with minimal latency, taking advantage of small price discrepancies across different exchanges or venues.

In this case, algorithms make split-second decisions. The intuition is to react quickly to market changes and capitalize on short-term price movements.

Quantitative trading firms and professionals often use a combination of mathematical optimization techniques, statistical analysis, machine learning, and computational power to develop and implement their trading strategies. These techniques help traders make data-driven decisions that can lead to improved trading performance and profitability.

Continuous Improvement

Trading optimization is an ongoing process. The intuition is to continually refine and adapt trading strategies as new data becomes available and as market conditions evolve.

In summary, the intuition behind optimization algorithms for trading is to use mathematical and computational techniques to find the best strategies and parameter settings that balance risk and reward, adapt to changing market conditions, and ultimately maximize returns for traders and investors.