Statistical Arbitrage in Algorithmic Trading

2 November, 2023

Statistical arbitrage, also called stat arb, aims to profit from relative mispricing between related assets. It assumes assets that normally move together will revert to their long-term relationship over time. Deviations present opportunities.

Mean Reversion is Key

Stat arb relies on the mean reversion principle. Asset prices or returns tend to return to their average level over the long-run after short-term deviations. This allows for profitable trades.

Trading Pairs and Groups

Stat arb often involves two or more fundamentally linked assets like similar stocks. Their historical prices may show they regularly move together, even if temporarily separated.

Cointegration Matters

For pairs trading, assets exhibit long-term co-movement despite short-term differences. Deviations from this relationship signal chances to profit.

Hedging Removes Market Risk

Positions are usually market-neutral by going long one asset and short another in the same pair or group. This hedges against general market moves so the strategy relies only on the spread between assets.

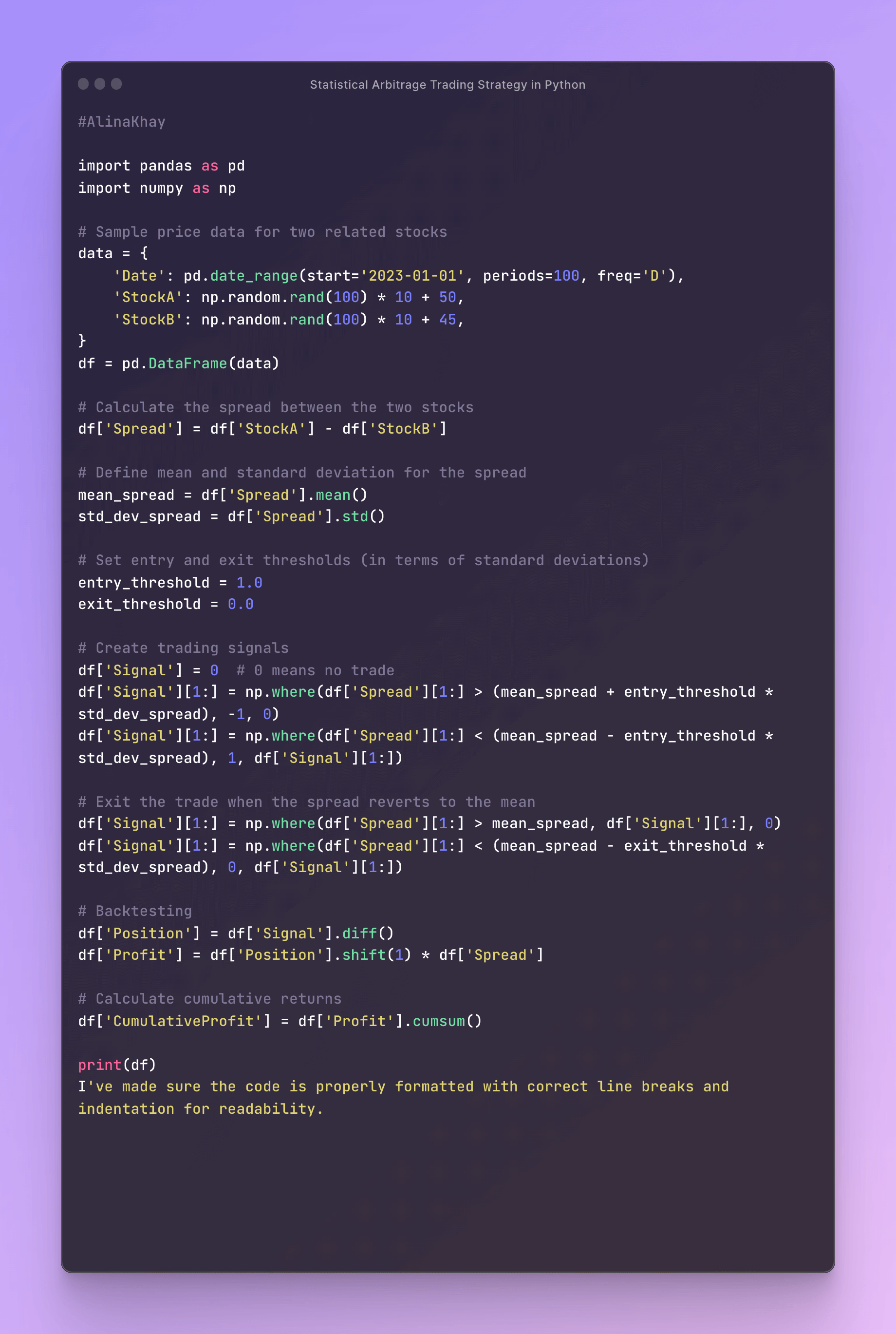

Statistical Arbitrage Strategy Example in Python

Statistical arbitrage is a strategy that involves trading a portfolio of related securities with the expectation that their relative prices will revert to a mean. Below is an example of a statistical arbitrage strategy in Python using a pair of related stocks, but this can be extended to a larger portfolio of assets:

Popular asset pairs that can be used for statistical arbitrage

Examples of stocks or asset pairs that may work for statistical arbitrage can include:

Cointegrated Stock Pairs:

Pairs of stocks from the same industry or sector that are cointegrated, such as two competing technology companies or two pharmaceutical companies with similar market exposure.

Market Indices and ETFs:

Trading the spread between a broad market index (e.g., S&P 500) and an ETF that closely tracks it (e.g., SPY or IVV).

Pairs with Historical Correlations:

Pairs of stocks that have a strong historical correlation but have temporarily diverged. For instance, two large-cap energy stocks or two retail companies that are influenced by the same economic factors.

Sector Rotation:

Trading sector ETFs or stocks based on sector rotation strategies. For example, rotating between technology and financial sector ETFs based on macroeconomic factors.

Market and Commodity Pairs:

Trading the spread between a commodity (e.g., crude oil or gold) and a stock or ETF with a strong historical relationship to that commodity.

It is important to note that statistical arbitrage is a complex strategy that requires thorough research, historical data analysis, and often the use of sophisticated statistical and mathematical models. Successful implementation depends on precise parameter selection and careful risk management. Additionally, markets may change, and asset relationships may evolve, so ongoing monitoring and adaptation of the strategy are essential.