Is Euphoria Over? Reading the Mid-July Regime Shift

And the Late Cycle Capital Rotation

The money hasn’t left the market; it has just stopped deciding that everyone deserves a share.

Markets rarely break in a single, clean sweep. Instead, they shift from a regime of unconstrained discovery to one of aggressive liquidity rationing. While the broader index might look deceptively flat and volatility appears contained, the tape has been pricing in a far less comfortable reality since early July.

Three superficially isolated headlines this month actually describe a single, interconnected process:

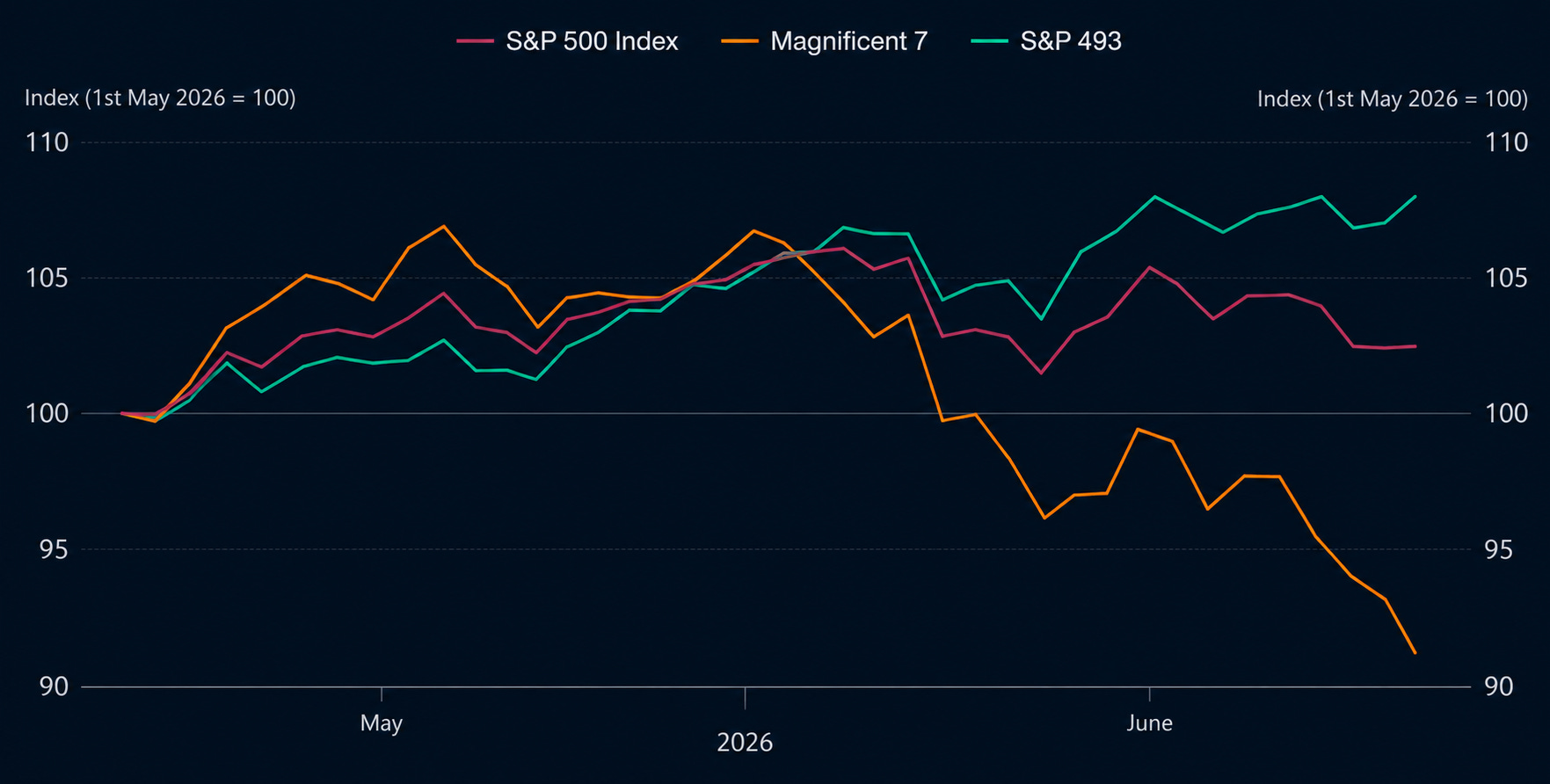

The $3.2 Trillion Reallocation: An unprecedented rotation where capital has fled highly crowded semiconductor stocks, pulling out of over-owned winners to seek shelter in the rest of the S&P 500 and cash-rich mega-caps.

The $SPCX Fracture: Weeks after the largest public debut on record, SpaceX ($SPCX$) slipped below its $135 fixed IPO floor to touch an intraday low of $132.15—a stark signal that the market’s capacity to absorb massive new supply is hitting a wall.

The CapEx Arms Race: Taiwan Semiconductor Manufacturing Co. (TSMC) lifted its capital expenditure forecast to an eye-watering $60B–$64B to keep building out AI infrastructure, raising the high-stakes question of who will ultimately fund the return on this massive cash burn.

Separately, these financial stories look as idiosyncratic events. Collectively, they reveal that the expansion regime is over, and a classic zero-sum game has begun.

When the pool of capital stops growing and hits a fixed boundary, laggards can only catch a bid if fresh assets are cannibalized from somewhere else. To navigate what comes next, we must look past daily index noise and analyze the dangerous internal cycling of a secular bull market starting to exhaust itself.