Mutual Fund Alpha

Mutual fund performance persistence, the "smart money" effect, and stock price momentum share a single root cause — and it has nothing to do with manager skill

A fund outperforms. Consultants update scorecards. Capital arrives. The manager does the rational thing: buys more of what she already owns. The stocks that made her look smart get bought again, by the same hands, with the new money her performance attracted. The price goes up. The track record extends. More capital arrives. At no point does anyone need to have been right about anything. The fund didn't beat because the manager has genuine edge. She beat it because she held the names that the next wave of capital would also buy. She surfed the flow, not the alpha. Capital chasing past performance is what created the returns, not manager skill.

What looks like skill persisting is capital self-reinforcing. And the data, when you disaggregate it carefully, is not kind to the alternative interpretation: fund alpha contains essentially zero incremental information about future performance once you control for the flow-induced demand embedded in the track record. The “smart money” rotating into last year’s winners isn’t smart — it’s the mechanism completing its own loop. Three anomalies the industry has monetised for decades turn out to share a single root cause, one that is observable in advance, and one that carries a reversal on a known schedule.

The reversal is predictable too — and the structural conditions that amplify it have deepened considerably since this observation was first quantified. The concentration has grown. The flows are larger. The mechanism is more legible than it has ever been, to anyone willing to read the plumbing rather than the press release.

The mechanism, precisely stated

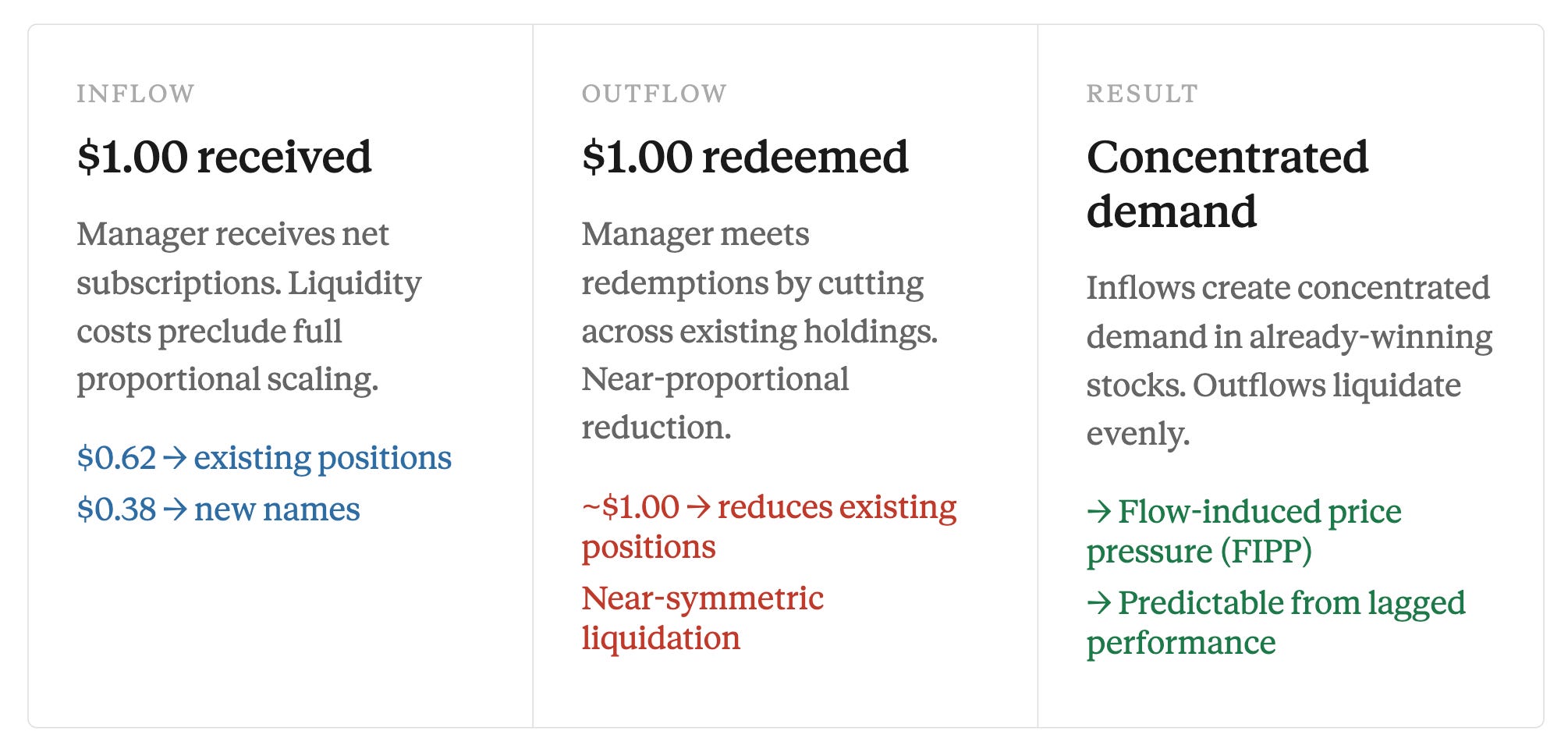

The mechanism starts with a simple observation about how fund managers respond to capital flows. If incoming money contains no information about which stocks to buy, rational managers should scale existing positions proportionally — maintaining target weights regardless of fund size. In practice, markets have friction, and scaling a large position by 20% in a single quarter is not the same operation as scaling a small one. Managers adopt an asymmetric response.

On redemptions, managers cut positions roughly dollar-for-dollar — forced selling to meet outflows. On inflows, the empirical scaling factor is 62 cents per dollar received: managers expand existing holdings partially, deploying the rest into new names to manage liquidity costs. This asymmetry is the mechanism’s engine.

FIPP - Flow-induced price pressure

The demand shock this creates — the FIPP variable — is both large and predictable. Large, because equity mutual fund gross flows exceeded $1.4 trillion annually even through the 2009 trough of the sample. Predictable, because fund flows chase past performance, and past performance is public and quarterly. A fund that outperformed last quarter will, on average, attract more capital next quarter. That capital flows into stocks already held by the outperforming fund — the same stocks that generated the outperformance to begin with. The loop is closed, traceable, and observable in advance.