Capturing the Systematic Edge When Volume Contradicts Price

Volume Is the Market’s Honesty Check on Price

Volume confirms price moves. That’s the first thing most traders learn, and it’s not wrong — it’s just incomplete. The more useful question isn’t whether volume is rising with price. It’s whether the volume justifies how far price moved. Those are different questions, and the gap between them is where the edge lives.

When price extends further than participation justifies, the market is borrowing against future conviction that may not arrive — a crowded position running in thin air, structurally vulnerable to reversal. When volume is heavy but price barely moves, the market is absorbing supply quietly — institutional demand meeting offered supply without moving the tape. One signals exhaustion. The other signals accumulation. Both are tradeable. Neither is visible in price alone.

In 2025, GLD has produced multiple sessions where True Range significantly outpaced participation — speculative extensions ahead of sharp reversals — while SLV has shown a different pattern: heavy volume, narrow range, quiet accumulation before the next leg. This is the framework that makes those sessions legible, and the exact setups that flow from each one.

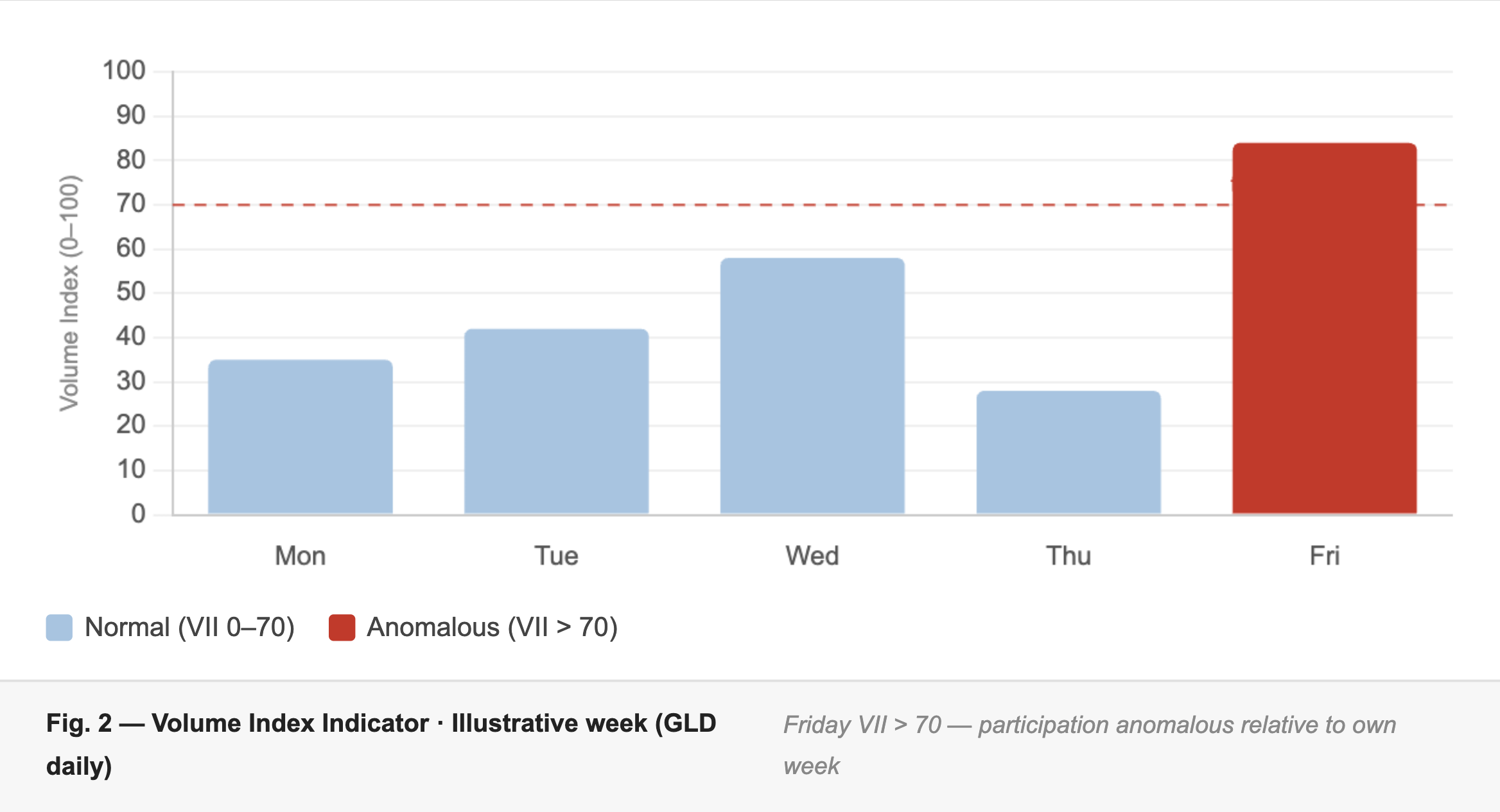

The Volume Index: Participation Relative to This Week

The 20-day Z-score solves the cross-instrument scaling problem. For reading intraday participation, you need something tighter: whether the current bar’s volume is anomalous relative to the past five days of this instrument specifically. The Volume Index Indicator (VII) provides that — it expresses the current bar’s volume as a percentile rank within the trailing 5-day window.

Volume Index Indicator (VII)

VII = (Volume_today − Volume_min[5d]) ÷ (Volume_max[5d] − Volume_min[5d]) × 100

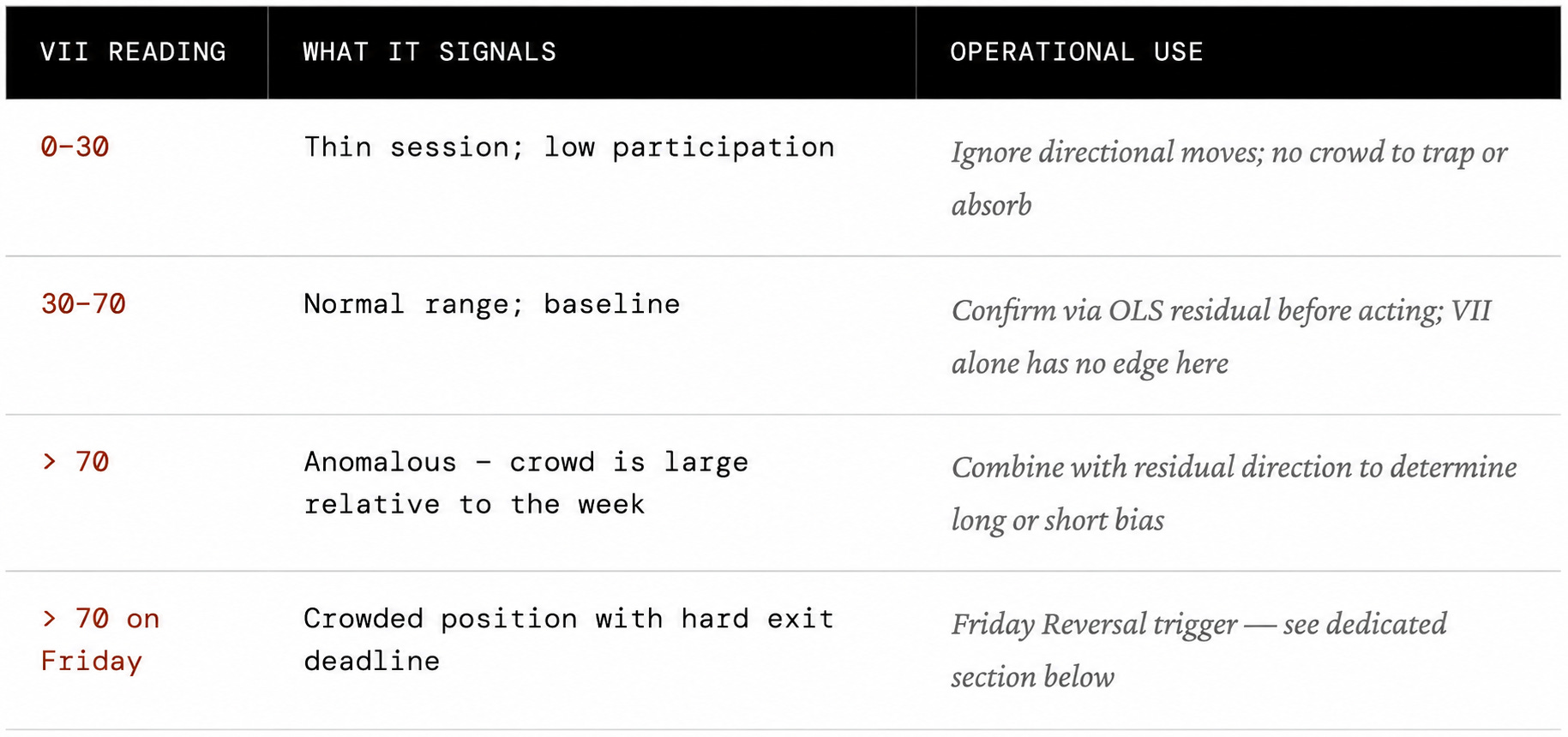

Range: 0 (lowest in 5-day window) → 100 (highest) · Anomaly threshold: VII > 70

A VII above 70 places current participation in the top 30% of the week’s range — anomalous relative to that instrument’s own recent baseline. This self-calibration is the point. A VII of 80 in a low-volume holiday week and a VII of 80 in a high-conviction macro week carry different weight in absolute terms; relative to their own window, both are equally anomalous, which is the operationally correct framing.