What Really Drives Gold Now

It isn't real yields

Real yields set the swings; central banks set the floor. Confusing the two is expensive.

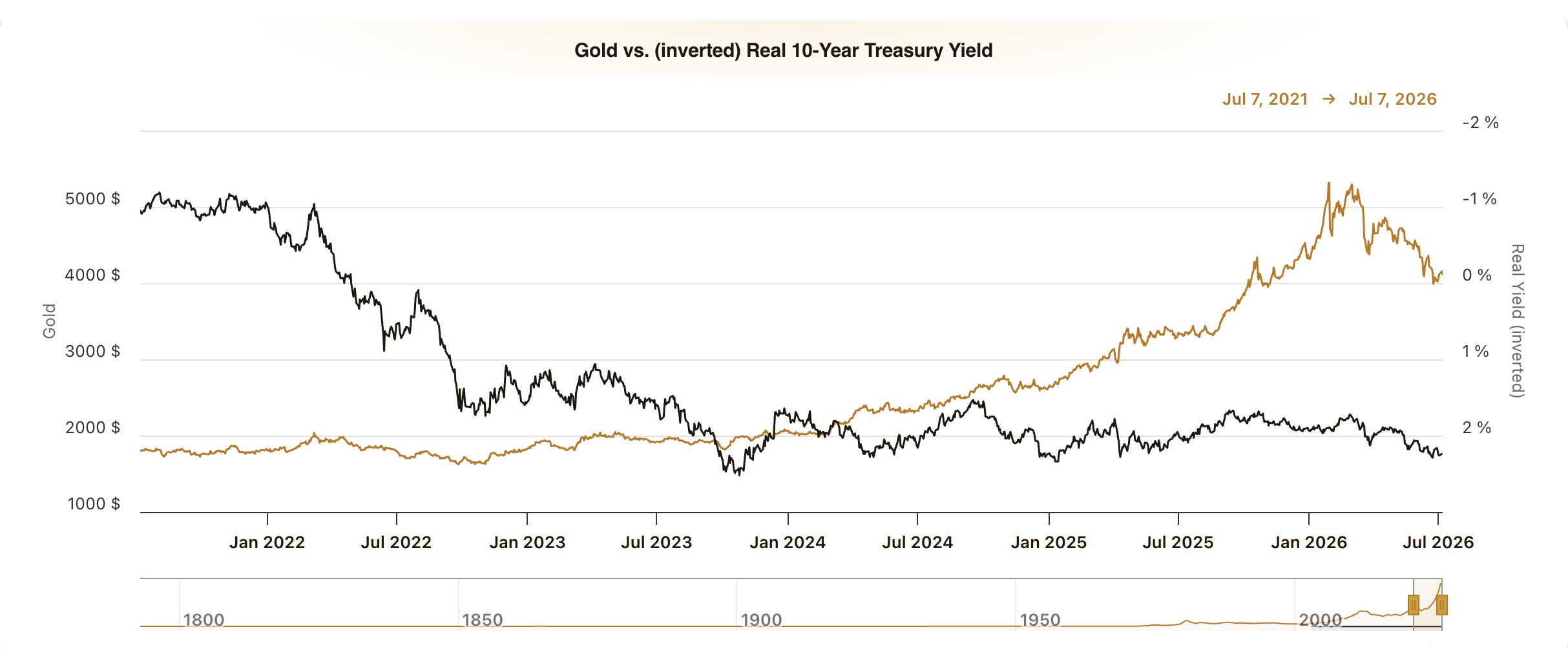

For two decades gold behaved like a mirror held up to real interest rates: yields up, gold down, with metronomic reliability. Around 2024 the mirror cracked. Gold returned some 65% in 2025, its best year since 1979, in the same twelve months that ten-year American real yields averaged close to 2%, their highest since 2007. The textbooks say these two things cannot happen together; rising real rates are supposed to be gold’s natural predator. Anyone still pricing the metal off the TIPS curve has been reading the wrong instrument.

The correction sharpens the question rather than settling it. Gold touched roughly $5,405 an ounce on the LBMA benchmark in January 2026, then gave back a hefty slice of the gain, trading near $4,170 by early July. Now that the momentum crowd has left the building, the awkward question is being asked out loud: what, exactly, is holding the price up?

Most trading desks still price gold off real rates, its old cyclical driver, and keep missing the level—because the buyer who now sets the price at the margin does not appear in that model at all. That gap is the argument of this piece. Sitting on the wrong side of it has been an expensive way to be theoretically correct.

There is a tidy way to take the metal apart: separate the part that sets the floor from the part that sets the amplitude. Do that, and 2025’s melt-up and 2026’s stumble stop looking like a contradiction. They run on different clocks—and most of the industry is still checking its watch against the fast one.

In fairness to the crowd

The real-rate model earned its reputation the honest way: it worked. From 2004 to 2021, gold traded like a very long-duration inflation-linked bond that had simply forgotten to pay a coupon. Regressed against the ten-year American real yield over that window, it carried an empirical duration of roughly 18 years: a 100-basis-point rise in real yields knocked about 18% off the inflation-adjusted price. The long-run correlation sat near minus 0.8. For the better part of a generation, knowing the TIPS yield was as good as knowing gold’s direction.

Then the relationship broke, and not politely. Through 2025, real yields sat at an eighteen-year high while gold rose by two-thirds. The model did not merely miss its forecast, it pointed the wrong way. What replaced it is a reserve-allocation story: a slow, structural, and dull grind—right up until the moment it shifts.