Where the Momentum Factor Still Works

What three decades of volatility data reveal about momentum’s true constraint

Momentum has been bleeding for a decade. The standard explanations - crowding, factor decay, regime change — have been recycled so many times they’ve lost meaning. Every year someone calls it structurally dead. Every year the evidence stays inconveniently ambiguous. But there is a cleaner read, and it comes from a place almost no post-mortem has looked: not whether the factor works, but whether the market is still moving at the speed the factor requires.

Before dismissing them: momentum is genuinely crowded in some asset classes like commodity trend-following, FX carry. It is decaying in others - volatility-targeting strategies in 2022. But in the one market where institutional momentum capital is deepest - U.S. equities - neither explanation holds. The crowding is unchanged from 2010, the decay is selective, not universal. This suggests the disease isn't momentum itself.

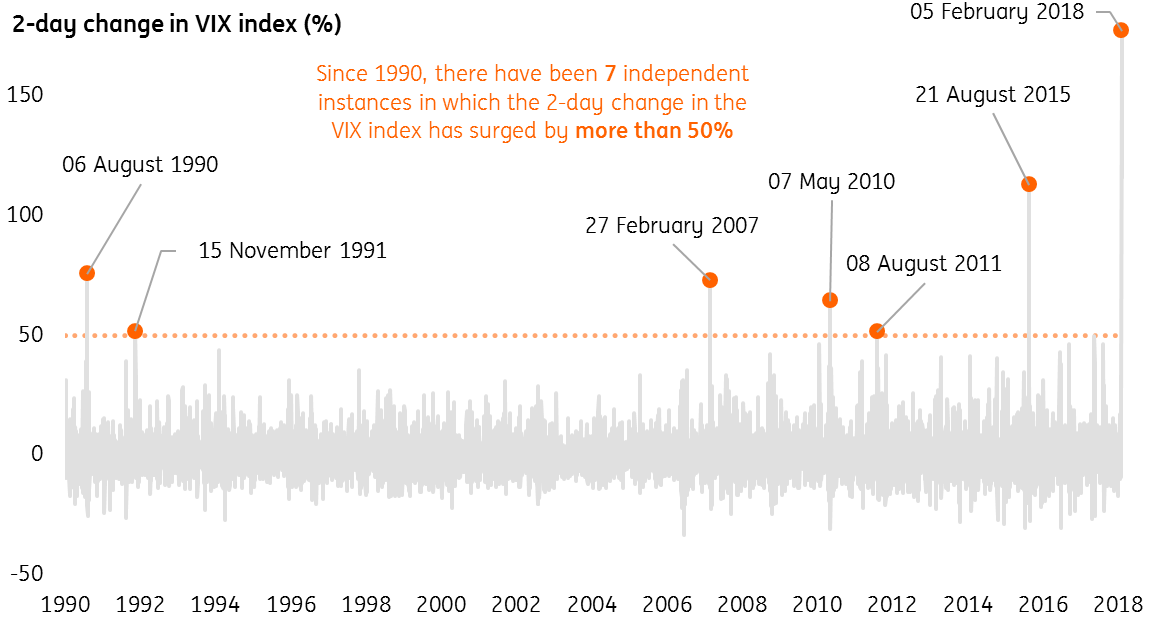

New research on three decades of VIX behaviour has an answer. It’s not the direction of volatility that broke momentum. It’s the tempo. And once you see how the two halves of that finding compound each other, the underperformance stops looking like a mystery and starts looking like arithmetic.

The mechanism is specific, the data is clean, and the position it implies is actionable. Here it is.

The consensus read is wrong in the right direction

Crowding doesn’t hold up.