Why the Rally Makes Sense Even If the World Doesn't

Four separate forces are all reading "risk on" at the same time, and their overlap explains why a war in the Gulf produced a new all-time high in the S&P 500. The consensus has the causation backwards

The S&P 500 sits 30% above its level twelve months prior, hitting new highs despite elevated geopolitical risk, weak consumer sentiment, and an oil shock hitting offshore economies. This looks irrational until you understand the four separate mechanisms underneath it.

The rally has four distinct engines running simultaneously. Each engine can fail independently. If one stalls, the other three can keep the rally alive. Two or three engines failing simultaneously ends the regime. Understanding which one is most vulnerable to reversal, and what that reversal looks like before it happens, is the trade. Most participants are watching all five as one undifferentiated “bull market.” That is the misread this piece is built around.

Engine I

The AI Earnings Cycle and Continued Momentum

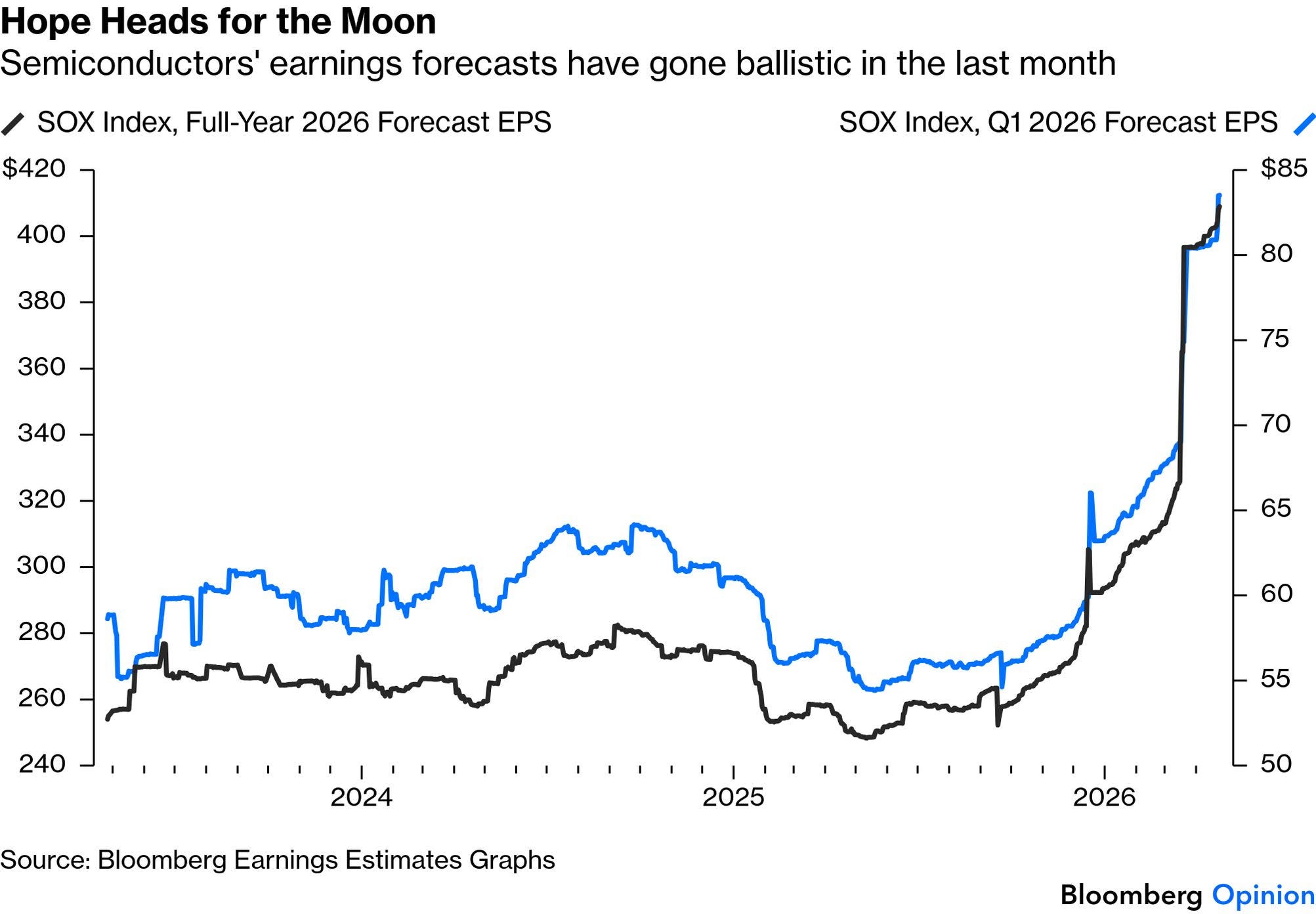

Start with the least controversial engine, because it is the one most people discount as “priced in.” It is not. Consensus earnings estimates for the S&P 500 have been revised higher for twelve consecutive weeks. Forward EPS now stands at $344 for the index, with 2027 consensus at $380 — numbers that were being called unreachable six months ago. Almost 80% of companies reporting Q1 2026 results beat analyst estimates, and in most cycles the beat rate falls once the year’s actual operating environment becomes clear. This time it is widening.

Semiconductor revenue is the lead indicator — the SOX has gained 47% in eighteen trading sessions, every session positive, the longest winning streak in the index’s history. But the important signal is not Nvidia, where the AI narrative has been consensus since 2023. It is the “blue-collar semi” complex: ON, STM, MCHP, TXN — analog and mixed-signal suppliers whose end markets are industrial equipment, automotive, and communications infrastructure. These chips do not go into language model training runs. They go into the machines that build the buildings that house the GPUs. Texas Instruments reported data center revenue up 90% year-on-year in Q1. That is not AI hype. That is construction cycle demand flowing through the industrial supply chain.

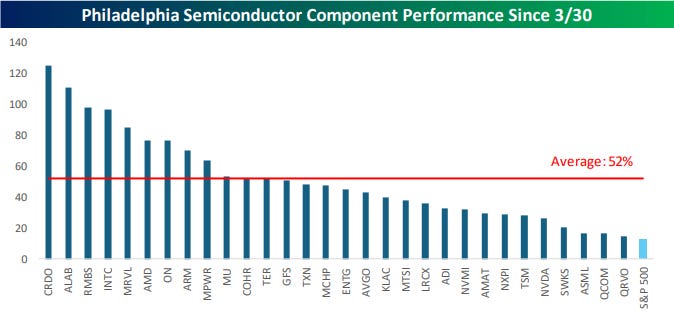

Broad strength in semiconductors is a structural signal. When all 30 stocks in an index outperform simultaneously, it's not concentrated hype—it's genuine demand distributed across the supply chain. Small-cap semis beat large-cap semis. This suggests capex isn't a Nvidia phenomenon, it's an ecosystem phenomenon. That's bullish for the thesis that the AI build-out is durable.

The investment-grade analogue is equally direct: investment-grade spreads have tightened 18 basis points since the war started. Credit is the senior claimant. When credit says “the cash flows are safe,” equities that look expensive on trailing multiples are, in many cases, rationally priced on forward cash flows under an accelerating AI capex cycle. The market P/E multiple has actually compressed from January levels because earnings grew faster than prices.

Engine II

The Geographic Energy Asymmetry

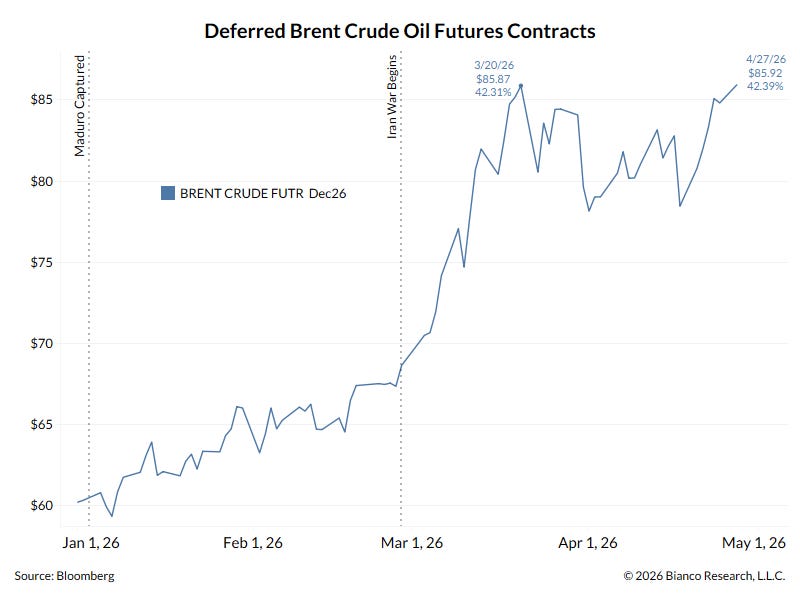

The U.S. produces 13 million barrels/day domestically. Europe and Asia do not. At $85 Brent, U.S. energy companies capture margin expansion while European/Asian economies face direct pass-through into growth headwinds. Capital fleeing energy-driven currency depreciation in EUR and JPY rotates into dollar assets. U.S. equities absorb the bid. This asymmetry is structural; the war only accelerates it.

This feeds into equity markets through two channels. The first is direct: US energy companies are capturing extraordinary margin expansion. The second is indirect: global capital seeking to escape energy-driven inflation and currency depreciation in Europe and Asia continues to rotate into dollar assets, which means US equities absorb the bid.